Return to My Accounts

Return to My Accounts

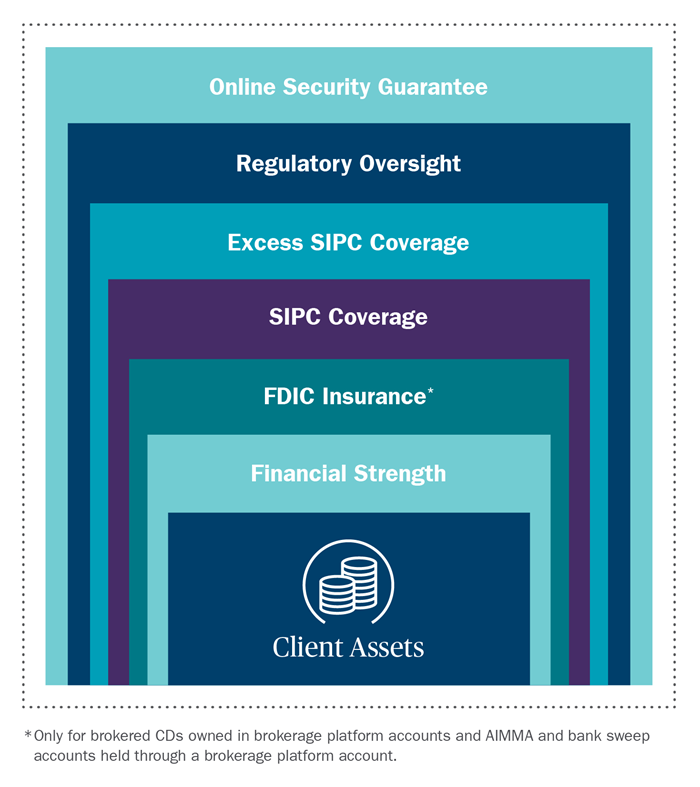

Understanding how your assets are protected

FDIC, SIPC and other types of protection

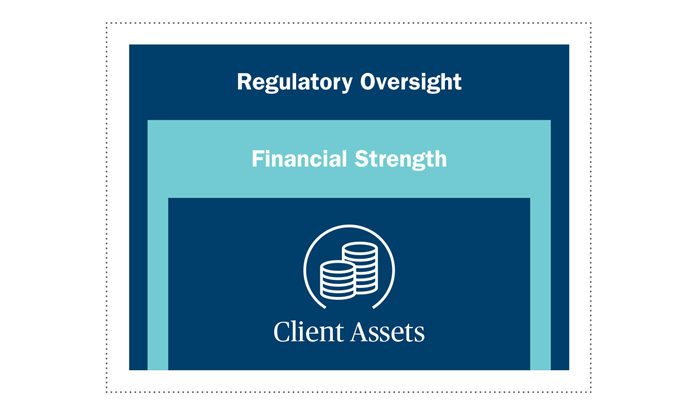

Ameriprise Financial is committed to protecting your assets. For more than 125 years, through good, volatile and unprecedented times, we’ve been there when our clients needed us. The strength of our commitment is matched by our strength as a company and all your assets held at Ameriprise are protected by that financial strength.

Below are just some of the other ways we look out for our clients, maintain a solid financial foundation, and run our business prudently within the regulatory environment.

Your assets held in brokerage and advisory accounts

The following types of protection covers these assets

Securities Investor Protection Corporation (SIPC) Coverage

SIPC has been protecting investors since 1970 and has over 3,500 securities brokerage firm members, which includes Ameriprise Financial Services, LLC and its clearing broker American Enterprise Investment Services, Inc (AEIS).

SIPC coverage provides protection to customers who hold cash and securities such as stocks, bonds or mutual funds in an account at SIPC-member brokerage firms in the event the brokerage firm fails. SIPC coverage applies if the brokerage firm goes out of business and your assets can’t be transferred to another brokerage firm because they were used in the operation of the failed firm.

Excess SIPC

Our brokerage accounts are also covered by supplemental "excess SIPC" insurance, which provides further protection to our clients (including up to $1.9 million for customer cash balances in a brokerage account), subject to an aggregate policy limit of $1 billion for all client claims. Review your Client Agreement to learn more about the SIPC insurance coverage specific to your Ameriprise® accounts. You can learn more about the SIPC by visiting its website at sipc.org

| SIPC protects your investments if: | SIPC does not protect: |

|---|---|

| Your brokerage firm is an SIPC member | Losses due to a decline in value of your securities |

| You have securities at your brokerage firm | Promises of investment performance |

| You have cash at your brokerage firm to buy securities | Commodities or futures contracts |

SIPC Insurance limits

Generally, SIPC covers up to $500,000 per account per brokerage firm, up to $250,000 of which can be in cash.

What if I have multiple accounts?

Protection of customers with multiple accounts at the same brokerage firm is determined by “separate capacity.” Each account, held by a customer in a separate capacity (e.g. individual, joint, IRA,etc) is protected up to $500,000 for securities and cash (including a $250,000 limit for cash only). Accounts held in the same capacity at the same brokerage firm are combined for purposes of the SIPC protection limits.

Neither FDIC nor SIPC coverage is provided for customers who have:

- Certificates (except for brokered CDs)

- Insurance products

- Mutual funds held directly with the mutual fund company (i.e., not in a brokerage account at Ameriprise Financial)

- Other “direct” investments, such as REITs, Limited Partnerships, or other securities for which AEIS does not provide custodial services

- Any assets held with non-FDIC or non-SIPC member institutions

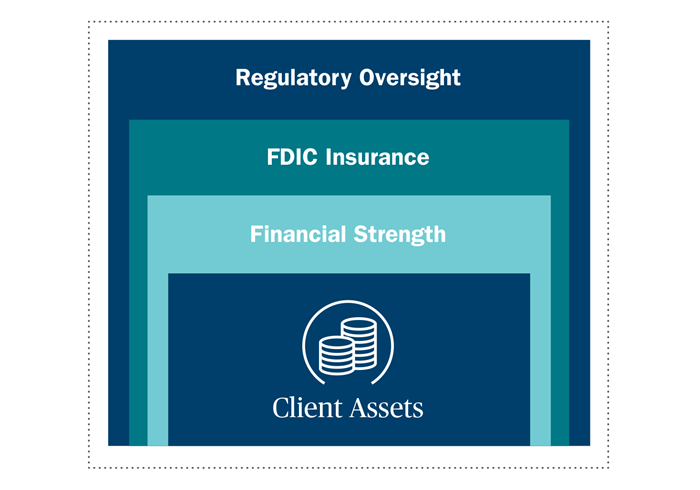

Federal Deposit Insurance Corporation (FDIC) Insurance

FDIC insurance covers brokered CDs owned in brokerage accounts and deposits in FDIC member federal banking institutions, such as banks and savings associations. FDIC insurance currently provides $250,000 per depositor, per insured bank, for each ownership category. Keep in mind, FDIC insurance covers all types of deposits received at an insured bank but does not cover investments.

| What the FDIC covers | What the FDIC does not cover |

|---|---|

| Checking accounts | Mutual funds |

| Savings accounts | Stock and bond investments |

| Money market deposit accounts | Life insurance policies |

| Certificates of deposit | Annuities |

| Cashiers checks, money orders and other official items issued by a bank | Municipal securities, U.S. Treasury bills, bonds or notes |

For cash held in an Ameriprise brokerage platform account, we offer most customers an FDIC-insured “sweep” account program. Our multi-bank program is called the Ameriprise® Insured Money Market Account (AIMMA). With AIMMA, Ameriprise transfers (or “sweeps”) brokerage account cash balances to multiple banks (possibly including Ameriprise Bank, FSB), each of which is FDIC-insured. Through AIMMA, clients are eligible to receive coverage for up to 10 banks for a total of $2.5 million in FDIC protection for cash in your brokerage accounts. Joint accounts are protected up to $5 million in cash.

Our single-bank program is called Ameriprise Bank Insured Sweep Account (ABISA). With ABISA, Ameriprise transfers or sweeps brokerage account cash balances to a single bank, Ameriprise Bank, FSB, which is FDIC-insured. Through ABISA, clients are eligible to receive up to $250,000 in FDIC protection for cash in brokerage accounts held within your qualified plan.

Examples of FDIC insurance limits

Single account holder

-

If you have $250,000 deposited in your name in an FDIC-insured bank, you are fully insured if the institution fails.

-

If you have more than $250,000 deposited in that bank, or if you have more than one account in your name at the same bank and the sum of your deposits exceeds $250,000, you are insured only up to $250,000.

Joint accounts

- A married couple can have up to $500,000 in one or more joint account(s) at the same insured bank and the deposits would be fully insured.

- Each spouse’s share of the joint account(s) is insured up to $250,000. If the couple has more than $500,000 deposited in one or more joint accounts, they are covered only up to $250,000 per owner for these joint accounts.

Multiple ownership type accounts

- If a married couple has a joint account at an FDIC-insured bank with a balance of $500,000, one spouse has an individual account at the same bank with a balance of $250,000, and the other spouse also has an individual account at that bank with a $250,000 balance, all of the deposits are covered. Each spouse is fully insured in their individual accounts, and the balance in the joint account is separately covered up to $250,000 each.

Retirement accounts

- Sometimes called qualified accounts, these accounts are also covered by FDIC insurance when the assets are deposited at an FDIC-insured bank. All retirement accounts, such as IRAs, SIMPLEs, SEPs and Keogh accounts, owned by the same person in the same FDIC-insured institution, are added together, and the total is insured up to $250,000.

Multi-bank Deposit Programs

- Certain types of accounts, such as the Ameriprise® Insured Money Market Account (AIMMA) multi-bank sweep program available to clients of Ameriprise Financial Services, LLC, provide clients with additional FDIC coverage because cash from their brokerage accounts is deposited in several different banks. Each AIMMA participant bank is insured by the FDIC, and each depositor’s cash deposit is insured up to the maximum of $250,000 at each bank. Once a client has $250,000 swept to a participant bank, additional cash in their brokerage account is deposited through AIMMA at another participant bank. Clients are responsible for monitoring the participant banks in which their cash is deposited through AIMMA to avoid exceeding FDIC coverage limits due to other deposit relationships they may have with those banks.

Because there are a number of banks in the AIMMA program, we can offer coverage on up to 10 banks which provides clients with up to $2.5 million in FDIC coverage in single-owner accounts. Joint accounts have up to $5 million in FDIC-insured cash, and retirement account holders can have up to $2.5 million in FDIC-insured cash.

Note: Online Security Guarantee provides some protection for activities not conducted by the client but through online trading or money movement.

All your assets held at Ameriprise are protected by regulatory oversight and our online security guarantee.

The brokerage and investment businesses of Ameriprise are also regulated by federal, state and other regulators.

Among other rules, we comply with the following:

- We can’t use your assets to run our businesses without your consent.

- You receive accurate records of brokerage account transactions, such as account statements and confirmations of transactions. For added safety, we keep all records in multiple secure locations.

- We maintain adequate levels of cash and liquid investments to meet our financial obligations to you.

Ameriprise Financial Services, LLC also ensures that:

- All our representatives are properly registered to conduct business.

- Our representatives have completed qualifying exams and annual continuing education requirements.

- All representatives are required to adhere to a strict code of conduct.

Regulatory oversight for insurance products and services

Ameriprise Financial offers insurance and annuity products and services produced by its affiliates, RiverSource Life Insurance Company and RiverSource Life Insurance Co. of New York. RiverSource has a long history of strength, stability and expertise and consistently receive high ratings from independent rating agencies.

Insurance and annuity product guarantees are subject to the claims-paying ability of the issuing company and are not insured by the FDIC or SIPC.

Rules for the insurance industry vary from state to state. Our insurance affiliates meet the requirements of each state in which they offer disability income, life insurance and annuity products, as well as the requirements of securities laws and regulations that apply to variable life insurance and annuity products.

We protect your personal information

Protecting your privacy and security is a top priority. That’s why we offer our Online Security Guarantee to ensure that your personal and account information are safe. It includes the following measures:

- We use industry-standard security methods, including firewalls, encryption and client authentication technology to control account access.

- You have the option of adding another layer of protection to your accounts with 2-Step Verification which increases your protection from fraud by helping to verify it is you logging into your account.

- The secure site on ameriprise.com protects the information you share with your advisor so it remains confidential.

The secure site also offers tools and resources that make it easy for you to securely view and manage your accounts. Your confidentiality is important, so we encourage you to protect your password and use up-to-date technology, including firewalls and anti-spyware, to protect your information.

We have safety measures for records and compliance

In addition to regulation and insurance coverage, Ameriprise Financial has the following measures in place:

- Safe securities holding — American Enterprise Investment Services, Inc. (AEIS) is the subsidiary responsible for trading, settlement and custody of cash and securities for brokerage clients of Ameriprise Financial. AEIS stores electronic records of securities in a central depository. This system is an industry standard which is considered safe and cost-effective. Unlike individual stock certificates, book-entry securities are less vulnerable to theft and can’t be counterfeited.

AEIS keeps records of each customer’s holdings and provides periodic statements that reflect current client positions. - Internal compliance staff — Ameriprise Financial has a dedicated compliance staff to help us stay current on regulatory requirements.

- Annual audits — An independent accounting firm conducts annual audits and provides an annual assessment of reported financials as well as the custody functions AEIS provides for customers’ brokerage assets. AEIS publishes a Statement of Financial Condition twice annually, available online at ameriprise.com/aeisfinancialstatement.

- Business continuity plan — This plan is designed to provide service to our clients during any significant disruptions of business operations. The plan includes contingency arrangements at our headquarters and at our data centers located in other parts of the country and is tested annually.