Is the housing market poised for a comeback in 2026?

Russell Price, Chief Economist – Ameriprise Financial

March 16, 2026

High borrowing costs and home prices kept existing home sales flat in 2025 and 2024, hovering at depressed levels not seen since 1995. But with potentially lower mortgage rates, could 2026 be the year that the housing market shakes off its sluggishness?

Here’s our 2026 housing outlook:

A more favorable backdrop for 2026

Housing market expectations are fairly optimistic as we head into the 2026 spring selling season. Overall, we forecast the market to grow by about 5% with prices generally flat year-over-year.

Here are a few dynamics that could work in the housing market’s favor:

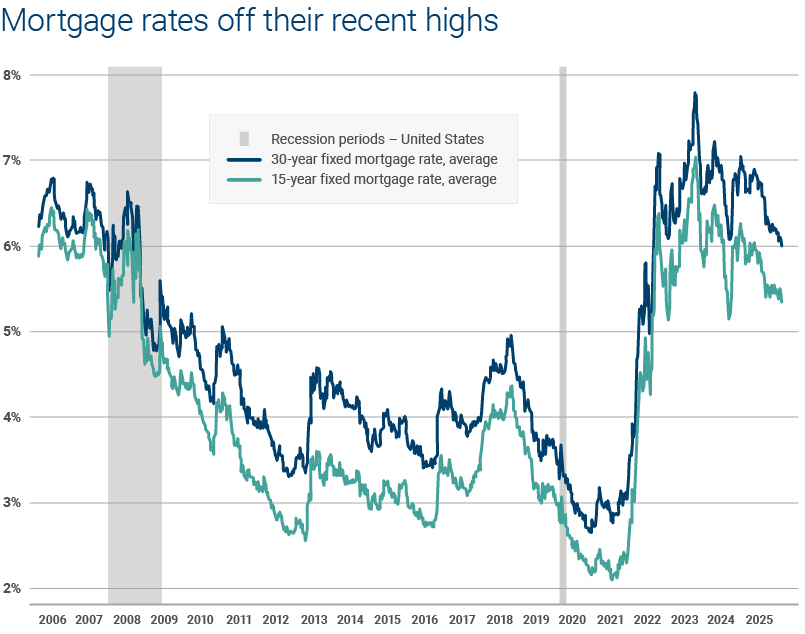

- Mortgage rates recently fell to three-and-a-half-year lows: For the first time since 2022, the average rate for a 30-year fixed-rate mortgage fell below 6.0% in February. While still above the rock-bottom rates of about 3% in 2021, lower rates could help boost affordability.

For example, for a $400,000 home with a 30-year mortgage rate of 7.0% with 20% down, the monthly mortgage payment would be $2,504. The current 30-year fixed rate of about 6.0% equates to a payment of $2,129, a savings of $375, or about 15%.

Source: FactSet Research Systems

- Home supply and demand are rising. The availability of homes for sale also appears to be increasing, and demand for pre-approved mortgages has been rising. In January, there were 1.1 million homes available for sale across the country, the highest level for any January since 2020.

- New limits on institutional buyers could improve availability for home buyers. A recent presidential executive order looks to limit the participation of institutional investors to a suggested 100 single-family housing units. Institutional buyers (defined as those owning 100 or more housing units) have been growing participants in the market for years. While institutional demand has no doubt helped support prices, it’s offered little room for improvement in affordability. Most estimates put institutional ownership at less than 5% of the housing stock, but market participation from the segment has, at times, been higher in recent years.

With mortgage rates near three-and-a-half-year lows, now may be a good time to consider refinancing your home loan. Explore the pros and cons of this financial move.

2026 opens on a slow note, but shows some positive signs

Against this optimism, it’s important to note that the housing market has begun the year with lackluster results, although there are some signs of a turnaround ahead of the spring selling season.

Here are a few data points to consider:

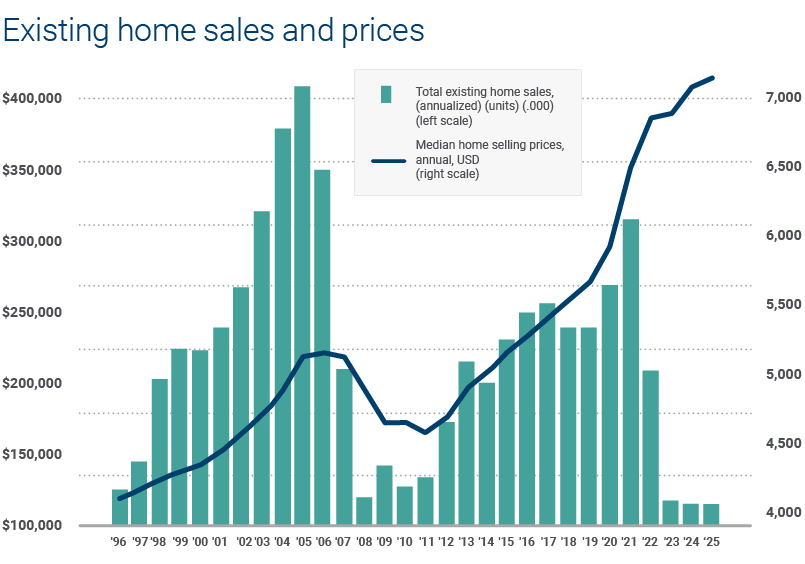

- Price gains have been weak. In January, the median price of existing homes sold was just 0.9% higher year-over-year, according to the National Association of Realtors.

- Sales started 2026 poorly. Particularly harsh winter weather across much of the country in January led existing home sales to a 4.4% decline versus year-ago levels, according to the National Association of Realtors.

- Prospective buyers seem ready for the spring selling season. Mortgage applications for home purchases jumped by more than 16% year-over-year in January, according to the Mortgage Bankers Association.

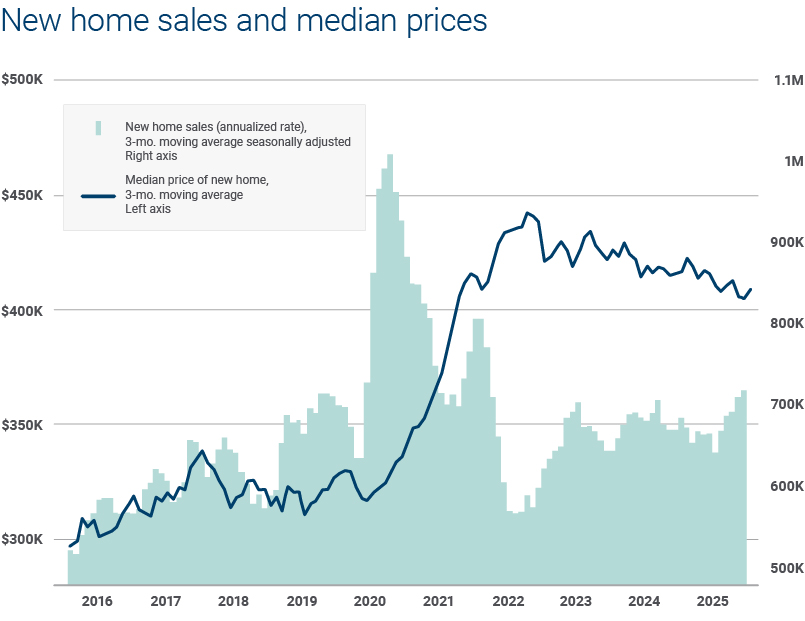

- New home sales were also basically flat in 2025 but are expected to see modest growth this year. Notably, new home sales gained momentum in the second half of 2025, with transaction volumes growing 5% year-over-year on average over the final five months of the year, according to data from the Census Department.

Source: FactSet Research Systems

Source: FactSet Research Systems

Bottom line: Better conditions, but still a year of recovery

Overall, we believe the U.S. housing market continues to recover from its “stickiness” of the last several years. Housing changed hands at a fast pace early in the decade when the Federal Reserve forced mortgage rates to multi-decade lows in support of the pandemic-impaired economy. As rates jumped higher in the years that followed, most property owners were reluctant to relocate because it would mean giving up an exceptionally low mortgage rate for one that was often double, or more, than their existing rate.

Such conditions are still in place, but as mortgage rates slowly moderate, affordability has been slowly improving. The itch to relocate also appears to be growing for a rising number of homeowners in a trend we believe should further aid the market’s recovery.

Understand how your home fits into your financial picture

For most people, their home is among the largest single financial assets in their portfolio. If you’re looking to buy, sell, refinance your mortgage or tap into your home equity, know that your Ameriprise financial advisor can help you understand the impact it may have on your broader financial situation.

Or, request an appointment online to speak with an advisor.

At Ameriprise, the financial advice we give each of our clients is personalized, based on your goals and no one else's.

If you know someone who could benefit from a conversation, please refer me.

Background and qualification information is available at FINRA's BrokerCheck website.