Return to My Accounts

Return to My Accounts

Annuities and taxes

If you have an annuity, there are different potential implications for your retirement savings and income based on the type of annuity you have and when you withdraw funds.

To make the most of an annuity, it’s important to consider their general tax rules.

In this article:

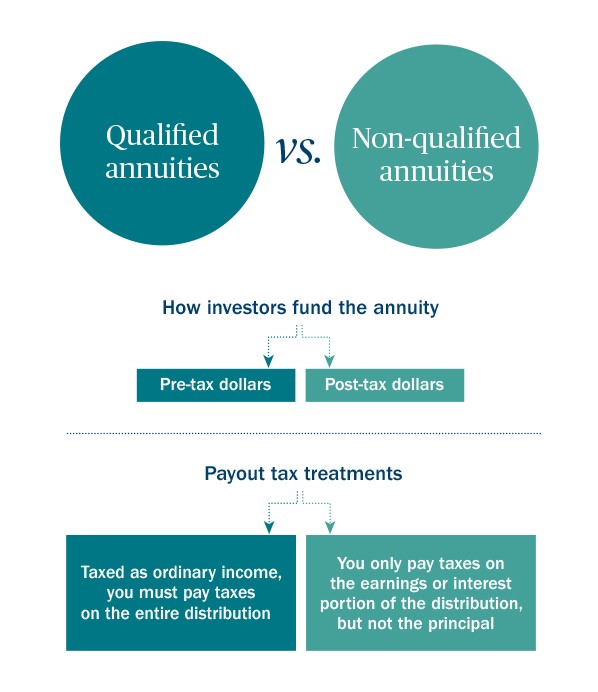

Taxation of qualified vs. non-qualified annuities: Key differences

Taxes are determined by the specific type of annuity you purchase -- either qualified or non-qualified. With a qualified annuity, you generally fund your annuity with pre-tax dollars, though Roth annuities are funded with after tax money. Non-qualified annuities are funded with post-tax dollars. This also affects the tax treatment of your payouts.

Taxation of qualified annuities

- Funding: Qualified annuities are generally funded with pre-tax dollars, however Roth annuities are funded with after tax money.

- Distributions: Qualified annuities are subject to required minimum distribution (RMD) guidelines unless it is a Roth IRA (Roth 401(k)s will no longer be subject to RMDs in 2024). You must begin taking distributions from a qualified annuity by April 1st of the year after you reach your RMD age, unless your annuity is in an employer-qualified plan and you are still working (and also not a 5% or greater owner of the business). The RMD age is 73 for individuals who turn 72 after 2022. Individuals who turned 72 prior to 2023 are already subject to RMDs. In 2033, the RMD age will increase to 75.

- Payouts: You will pay normal income taxes on the entire distribution amount. Annuities purchased with a Roth IRA or Roth 401(k), however, may be tax free if specific requirements are met.

- Other considerations: If you invest in an annuity to fund a retirement plan or an IRA, the annuity will not provide additional tax deferral benefits for that retirement plan or IRA plan.

Taxation of non-qualified annuities

- Funding: Non-qualified annuities are funded with post-tax dollars and grow tax deferred.

- Distributions: Non-qualified annuities are exempt from required minimum distribution guidelines. Once you start taking distributions from a non-qualified annuity, any interest or earnings within the annuity will be distributed before the premium or principal amount.

- Payouts: The interest (or earnings) are taxed as ordinary income but you won’t pay taxes on the premium or principal you initially deposited.

Annuity early withdrawal penalties

An annuity can be a smart addition to your retirement plan, but it’s important to keep in mind that if you make a withdrawal prior to the designated time period, you can expect to pay early withdrawal penalties on your annuity.

- Annuity withdrawals made before you reach age 59½ are typically subject to a 10% early withdrawal penalty tax. For early withdrawals from a pre-tax qualified annuity, the entire distribution amount may be subject to the penalty. If you withdraw money early from a non-qualified annuity, typically only earnings and interest will be subject to the penalty.

- While there aren’t many exceptions to the 10% early withdrawal penalty, you can explore potential options with your tax advisor that may be available to you based upon your individual circumstances.

- In addition to potential tax penalties, withdrawals may also be subject to surrender charges by the annuity issuer. This may happen if the amount withdrawn exceeds any penalty-free amount during the surrender charge period. Surrender charges vary by the annuity product you purchase, so make sure to check with the annuity issuer before withdrawing money from an annuity.

If you are considering withdrawing from your annuity early, it’s a good idea to speak with a tax professional.

An Ameriprise financial advisor can help

Annuities can offer steady income and tax benefits making them a popular way to save for retirement. There are a variety of annuity products available to help meet retirement savings and income needs. An Ameriprise financial advisor can review your individual financial situation and partner with your tax professional to evaluate your annuity tax strategy.

Or, request an appointment online to speak with an advisor.

At Ameriprise, the financial advice we give each of our clients is personalized, based on your goals and no one else's.

If you know someone who could benefit from a conversation, please refer me.

Background and qualification information is available at FINRA's BrokerCheck website.

This information is being provided only as a general source of information and is not a solicitation to buy or sell any securities, accounts or strategies mentioned. The information is not intended to be used as the sole basis for investment decisions, nor should it be construed as a recommendation or advice designed to meet the particular needs of an individual investor. Please seek the advice of a financial advisor regarding your particular financial situation.

Before you purchase, be sure to ask your financial professional about the annuity’s features, benefits, risks and fees, and whether the annuity is appropriate for you, based on your financial situation and objectives.

Most annuities have a tax-deferred feature. So do many retirement plans under the Internal Revenue Code. As a result, when you use an annuity to fund a retirement plan that is tax-deferred, your annuity will not provide any necessary or additional deferral for that retirement plan. But annuities do have features other than tax deferral that may help you reach your retirement goals. You should consult your tax adviser prior to making a purchase for an explanation of the tax implications.

Withdrawals that do not qualify for a waiver may be subject to a withdrawal charge. Withdrawals are subject to income taxes and withdrawals before age 59-1/2 may incur an IRS 10% early withdrawal penalty.

Ameriprise Financial, Inc. and its affiliates do not offer tax or legal advice. Consumers should consult with their tax advisor or attorney regarding their specific situation.

Investment products are not insured by the FDIC, NCUA or any federal agency, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Ameriprise Financial Services, LLC. Member FINRA and SIPC.