Return to My Accounts

Return to My Accounts

Paying for college: Financial steps to take as school nears

Learn how to pay for college tuition and costs as your child applies to school and prepares to embark on their higher education journey.

It’s time. After years of planning for this important financial goal, your student’s college years are right around the corner. Among the many decisions you’ll make, a strategy for how to pay for college costs is critical. Your options may include savings, investments, financial aid, scholarships and potential loans.

As you and your student prepare, an Ameriprise financial advisor will help evaluate your choices, offer guidance on tax strategies and the FAFSA and help determine what is fitting for you and your long-term goals.

Here are key steps to consider ahead of your first tuition payment.

In this article:

- Bring your assets into focus

- Have a family conversation about college finances

- Fill out the FAFSA — regardless of your income level

- Consider your financial aid packages and third-party scholarships and grants

- Decide on student loans

- Decide how you’ll make tuition payments

- Consider taxes in your payment plan

- Set your student up for success

- Questions to ask an Ameriprise financial advisor

1. Bring your assets into focus

Before you finalize your financial plan for paying for college, take an inventory of your 529 plan balances and other expected funding sources — such as savings and investments — to determine the total amount you plan to contribute to your student’s education. Also consider how other contributions — such as gifts from grandparents — may come into play as you evaluate your options to pay for college tuition.

- Learn more: College savings calculator

- Learn more: Saving for college: What to know about your options

- Learn more: 529 plans: Frequently asked questions

2. Have a family conversation about college finances

The college selection process is a good time to discuss the college experience your student wants to have as well as the financial implications of your student’s specific college choices. Start with your college budget and any potential contribution from your student that you agree on.

As they submit applications, consider the projected costs of their top choices. Each school is required to have a net price calculator on its website where you can get a breakdown of the real cost of attendance. The net price calculator can provide an estimate for what your family may pay for tuition instead the sticker price, before you receive a financial aid package.

3. Fill out the FAFSA — regardless of your income level

Key to receiving financial aid is filling out the Free Application for Federal Student Aid (FAFSA), which is used to determine aid from the government and most colleges and universities. Because multiple factors determine eligibility for aid under the FAFSA, submit it even if you assume your family’s income is too high to receive any form of aid. The information provided to the FAFSA is also used to obtain a variety of non-need-based federal loans, and many schools require the FAFSA to determine merit-based aid included in your financial package.

4. Consider your financial aid packages and third-party scholarships and grants

After you receive financial aid award letters, review the packages and related expenses of your student’s top choices. Your child’s financial aid package may include scholarships, grants and work-study. But there are additional opportunities outside of this package that your child may be eligible for.

Various scholarship-finder websites can help you identify opportunities based on financial need, merit, community service, heritage, gender, sexual orientation and life experience. Some also benefit students who have unique skills and hobbies.

- Learn more: College financial aid basics

5. Decide on student loans

Now that you have a projected budget, you can determine whether a loan is the right option for your family. Perhaps you'd like your child to take out a federal loan so they have a role in financing their education and can establish a credit history. For these reasons, this may be a better option than extending a personal loan to your student.

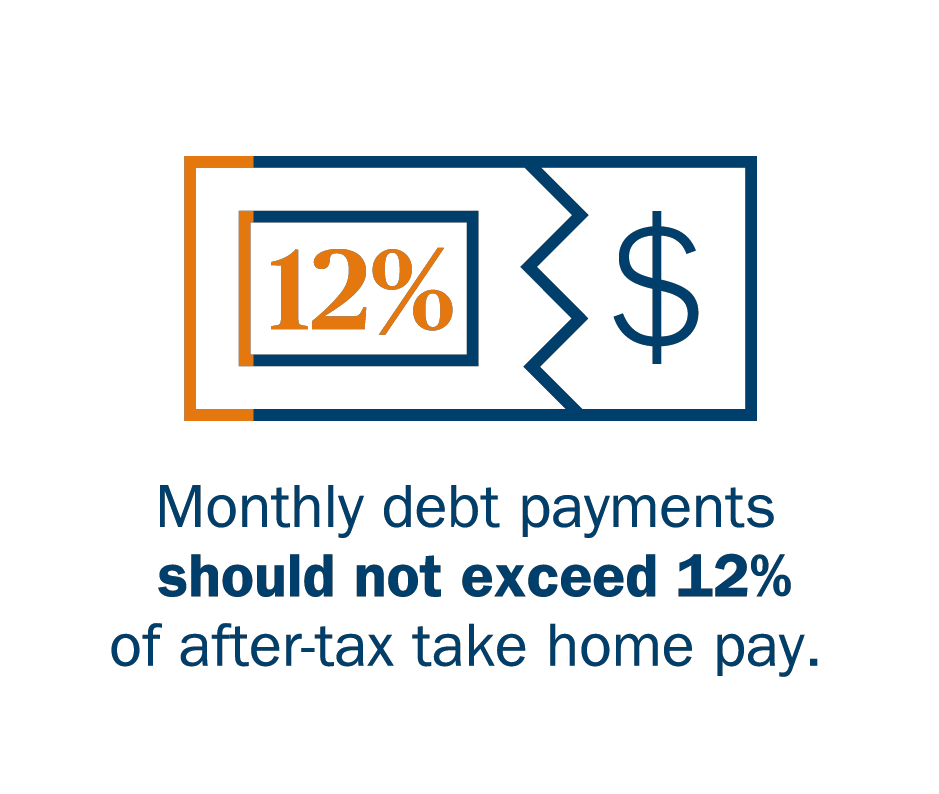

There are many different financing options, so plan to carefully weigh the pros and cons of each. If you and your student decide to borrow, you can help them fully understand the terms. A general guideline to consider is that the student’s projected total salary after graduation should be equal to or greater than 1.5 times the student loan balance. Monthly debt payments should not exceed 12% of after-tax take home pay.

Advice spotlight

Be strategic about the loans your family takes out.

For some families, it may make sense to take out a short-term loan and then pay it off with investments, such as short-term, high-yield instruments, that may appreciate at a faster rate.

- Learn more: Student debt and college loans, explained

6. Decide how you'll make tuition payments

When the time comes to write a check to your student’s school, determine the details of how you want to pay college tuition: a lump-sum payment or installments. A tuition payment plan, offered by many higher education institutions, will help you do the latter. This option may be attractive because it allows you to make regular payments over a fixed period, such as the academic year or semester. However, there may be a fee to enroll in such plans.

If a grandparent or other family member is helping fund your student’s education, they may want to take advantage of the tuition gift tax exclusion, which can help reduce their taxable estate.

Advice spotlight

Payments made directly to a school are exempt from the gift tax and can help lower the taxable value of an overall estate.

Under the gift tax exclusion rule, tuition payments made directly to a college are not considered gifts for tax purposes, nor are they counted toward the annual gift tax exclusion or the $12 million lifetime gift tax exemption. This exclusion only applies to tuition payments and not other expenses like books, supplies or room and board.

7. Consider taxes in your payment plan

As you pay for college, consider all tax implications. Federal incentives like the American Opportunity Tax Credit, Lifetime Learning Credit and student loan interest deduction can be leveraged, if applicable, to offset education costs. But make sure to coordinate your 529 plan withdrawals with these credits. Tuition expenses paid with tax-free 529 plan funds are not eligible for a tax credit.

- Learn more: Tax strategies for college savings and gifting

8. Set your student up for success

Before your student heads off to school, consider talking about budgeting in college and how to manage their expenses as young adults. For many students, college is full of new experiences, financial independence being one of them.

When you’re ready to reach out to an Ameriprise financial advisor for a complimentary initial consultation, consider bringing these questions to your meeting.

Something went wrong. Do you want to try reloading? Try again

Get help evaluating your options for paying for college

From tax strategies to FAFSA guidance, an Ameriprise financial advisor will help you make informed decisions about paying for your student’s school, while staying on track for other long-term goals, like retirement.

RELATED INFORMATION

Or, request an appointment online to speak with an advisor.

At Ameriprise, the financial advice we give each of our clients is personalized, based on your goals and no one else's.

If you know someone who could benefit from a conversation, please refer me.

Background and qualification information is available at FINRA's BrokerCheck website.

Ameriprise Financial cannot guarantee future financial results.

Clients contributing to a 529 Plan offered by a state in which they are not a resident, should consider, before investing, whether their, or their designated beneficiary(s) home state offers any state tax or other state benefits such as financial aid, scholarship funds or protection from creditors that are only available for investments in such state’s qualified tuition program.

The earnings portion of money withdrawn from a 529 plan that is not spent on eligible expenses will be subject to income tax, an additional 10% federal tax penalty, and the possibility of a recapture of any state tax deductions or credits taken.

Ameriprise Financial, Inc. and its affiliates do not offer tax or legal advice. Consumers should consult with their tax advisor or attorney regarding their specific situation.

By clicking the link to the net price calculator, you will leave ameriprise.com. The included hyperlink is provided for informational purposes only and is not an indication or endorsement of the content therein or affiliation with respect to the linked site. Be aware that the linked site will be subject to rules, regulation, and privacy and security provisions that are separate, and may differ, from Ameriprise Financial.

The initial consultation provides an overview of financial planning concepts. You will not receive written analysis and/or recommendations.

Investment products are not insured by the FDIC, NCUA or any federal agency, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities offered by Ameriprise Financial Services, LLC. Member FINRA and SIPC.