AI is carrying the market. But can the consumer keep up?

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — MAY 11, 2026

The S&P 500 Index and NASDAQ Composite logged their sixth straight week of gains last week, driven by strong AI momentum, outsized earnings growth and stable employment conditions. This week, April inflation reports and an update on retail sales will take center stage.

Last week in review:

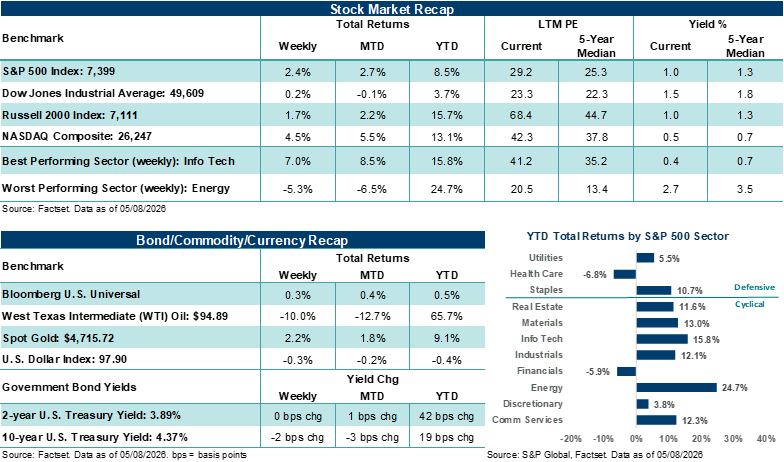

- The S&P 500 gained +2.4% last week and is now up over +16% in the last six weeks, its best run in the past 15 years.

- The NASDAQ Composite finished higher by +4.5% last week, up over +25% in the last six weeks, its second-best run since May 2001, only trailing the consecutive winning streak seen in the early days of the Great Financial Crisis rebound.

- The Dow Jones Industrial Average ended higher by +0.2%, and the Russell 2000 Index gained +1.7%.

- Treasury prices were little changed. The U.S. Dollar Index moved lower. Gold ended higher, and crude moved lower.

- A potential U.S./Iran framework, a solid jobs report, and AMD doubling its long-term chip opportunity delivered a rare convergence of catalysts across geopolitics, the economy and earnings that pulled sidelined cash into equities.

- On the other hand, markets are pricing in a diplomatic Iran resolution that doesn't exist yet, riding a tech rally where semiconductors are more extended than at any point outside of March 2000, and leaning on a consumer that's absorbing a massive rise in gas prices while sentiment sits at record lows.

“The fundamental backdrop for stocks is rarely this supportive, and the AI trade has reasserted itself as the dominant market force. The broadening of the semiconductor rally, the scale of hyperscaler spending commitments and upward revisions to the profit outlook all give investors a strong forward-looking growth narrative that is difficult for the bears to sell against. We believe this engine is the principal reason stocks sit at all-time highs today.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

AI is carrying the market. But can the consumer keep up?

Last week’s updates gave investors a deeper look into the two major engines driving this market, and, in our view, they revealed that each is running at very different speeds.

Last week, we asked: "How far can one engine take the market?" We noted the artificial intelligence engine was running at full strength while the consumer engine "might be starting to run low on fuel," and that last week's employment data would help determine whether the rally had room to extend. Well, investors got their answer, and as is often the case, the story is nuanced.

On the AI side, the investment cycle continues to accelerate. The rally across semiconductors, which has been the dominant force behind the market's recovery from the March lows, took another step forward last week with a round of earnings reports that again confirm AI demand is broadening across the supply chain. For example, AMD reported data center revenue growth of +57% in Q1, with forward guidance that came in above expectations. The stock jumped roughly +26% last week. In addition, Arm Holdings posted record revenue, with central processing unit (CPU) demand exceeding initial forecasts by more than double. And Intel, which beat profit estimates the prior week, reinforced the theme with data center chip sales rising +22%. Importantly, the AI semiconductor narrative is now broadening beyond just graphics processing units (GPUs) and into CPUs as the AI infrastructure buildout deepens.

And the spending commitments behind this infrastructure cycle are equally notable. Combined capital expenditure budgets among the largest U.S. hyperscalers (i.e., Microsoft, Google, Amazon, and Meta Platforms) are on pace to exceed $700 billion this year, well beyond 2025 levels. Every major cloud provider has signaled that AI infrastructure remains supply-constrained, not demand-constrained. Simply put, it likely means the investment cycle has a demand floor that extends well beyond the current quarter, which is why investors have quickly used the March lows to reallocate back into Technology.

As we have noted over recent weeks, the current earnings season has been remarkably strong. With roughly 89% of S&P 500 companies having reported, Q1 earnings per share (EPS) growth is tracking near +28% year-over-year, more than double analysts' expectations at the start of the quarter. Notably, the beat rate is running at a very impressive 84%, the highest since Q4’21 according to FactSet, and net profit margins have expanded to record levels. Importantly, S&P 500 EPS estimates for the coming quarters have been revised higher, with Energy and Technology seen leading profit growth. Full-year 2026 earnings growth is now tracking at +21% year-over-year, which would represent the strongest calendar year for corporate profits since 2021. Bottom line: The fundamental backdrop for stocks is rarely this supportive, and the AI trade has reasserted itself as the dominant market force. The broadening of the semiconductor rally, the scale of hyperscaler spending commitments and upward revisions to the profit outlook all give investors a strong forward-looking growth narrative that is difficult for the bears to sell against. We believe this engine is the principal reason stocks sit at all-time highs today.

So, what about the other engine? Here, the consumer side of the economy is telling a more complicated story, and those engine knocks we flagged last week could grow louder over time. On the surface, the April nonfarm payrolls report delivered a solid result. Job growth came in at +115,000 last month, well above expectations of 65,000. But the composition of job gains also matters. Healthcare, transportation and retail accounted for the bulk of the gains, while information, financial activities, and manufacturing all contracted. Thus, the job data last week showed that hiring is narrowing into needs-based, defensive sectors. Also, wage growth came in below expectations at +0.2% month-over-month, and when stacked against inflation still running above +3.0%, real wage growth is anemic. Bottom line: Workers are not gaining purchasing power. Labor force participation fell to its lowest level since late 2021. And the underemployment rate (i.e., U-6) ticked higher, with part-time employment for economic reasons jumping by +445,000 in April (though year-to-date figures remain below late-2025 levels).

Consumer sentiment is also not very encouraging right now, even after accounting for established political biases in surveys. For example, the preliminary May reading from the University of Michigan Consumer Sentiment Survey again moved lower, breaking April's record to become the lowest reading in the survey's 74-year history. Current conditions collapsed by nearly 5 points, one of the largest single-month declines on record. Of course, that doesn’t mean the consumer is collapsing. But expectations in the latest survey barely budged, and, notably, inflation expectations moved lower. Thus, consumers say the present feels worse, but at the same time, they don’t expect conditions to get worse. Helping weigh on consumer sentiment is the fact that gas prices averaged $4.55 per gallon last week, the highest level since 2022, according to AAA, and are up more than 50% since the conflict began. With the personal savings rate moving to a three-year low in March and mixed signals on the labor front, consumers’ buffers might be thinning as price pressures take hold.

On the earnings front, consumer signals also show some signs of stress. McDonald's beat Q1 estimates, but its CEO warned the environment is "certainly not improving, and may be getting a little bit worse," flagging elevated gas prices as a disproportionate burden on lower-income consumers. The company responded by expanding its value menus to defend market share. And Shake Shack missed on both the top and bottom line, swung to an operating loss in Q1, and saw its stock fall nearly 29% last week. Higher input costs and weaker foot traffic in urban markets were the culprits.

Further, research last week from the New York Federal Reserve added important context on the current state of the consumer, in our view. The gas price shock stemming from the U.S./Iran conflict has produced a “K-shaped” consumption pattern that, in the Fed's own words, is "quantitatively larger" than the 2022 Russia/Ukraine commodity shock. For example, households earning below $40,000 annually have cut gas consumption by roughly 7.0%. Conversely, households with annual income above $125,000 have cut gas consumption by just 1.0%. Bottom line: We believe higher commodity prices are quietly widening the income divide and functioning as a regressive tax that hits the most stretched consumers the hardest.

Taken a step further and applying last week’s updates to our two-engine analogy, the AI cycle appears to be benefiting asset-exposed, higher-income households through the wealth effect. At the same time, the current energy shock appears to be pressuring lower-income households through higher gas prices, higher grocery costs, and eroding purchasing power. And with energy costs feeding into inflation, the Federal Reserve remains constrained to some extent, even if a rate cut or two is unlikely to help the most stretched households over the intermediate term.

From our vantage point, the AI engine is running at full throttle, particularly off the March lows. Earnings are strong. The AI investment cycle is broadening. And we believe the worst-case U.S./Iran outcomes remain less likely today, given that diplomatic channels remain active. As such, we believe the consumer engine is where the risks are quietly building. Simply, the price direction of oil and commodities is a meaningful variable that could determine whether those risks stay manageable or become something the market can no longer ignore. For long-term investors, we believe the environment supports staying invested and maintaining diversification. But we believe both engines need to keep running for this market to sustain its current pace. For now, the AI side is doing its part. The question is whether the consumer can do the same, particularly if problems in the Middle East persist or the AI trade unexpectedly loses some steam.

The week ahead:

- April CPI lands Tuesday and will provide a read on whether Iran-conflict-driven inflation pressures continue to build.

- April retail sales on Thursday will update the consumer spending picture amid high gas prices and record-low sentiment.

- Applied Materials and Cisco headline the earnings slate, offering reads on semi capex and enterprise spending.