Setting up this week’s “All In Wednesday”

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — APRIL 27, 2026

The S&P 500 Index and the NASDAQ Composite posted a fourth consecutive weekly gain, both closing at fresh all-time highs, as a strong earnings season, AI-driven semiconductor strength and the ongoing durability of the Iran ceasefire kept investor sentiment broadly constructive. This week, the FOMC meeting on Wednesday takes center stage, alongside first-quarter GDP, March PCE and a heavy slate of Magnificent Seven earnings reports.

Last week in review:

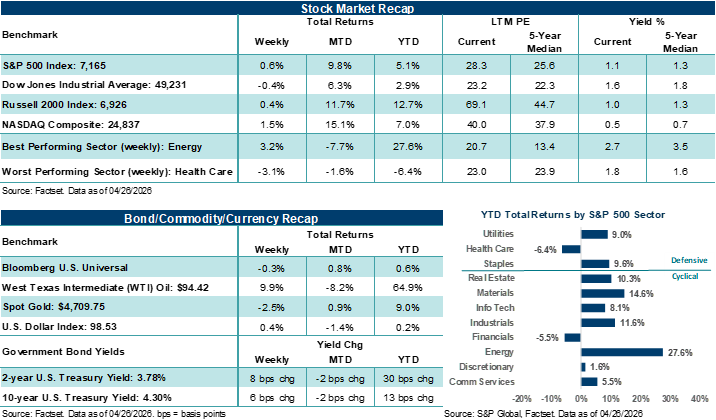

- The S&P 500 gained +0.6%, closing at a record high, while the NASDAQ rose +1.50%, also finishing at a fresh all-time high. The Russell 2000 advanced +0.4%, its fifth straight weekly gain, and the Dow Jones Industrial Average dipped 0.4%. Notably, breadth was narrow across the major averages, with the equal-weight S&P 500 falling 0.6%.

- Energy and Technology led all S&P 500 sectors, gaining +3.2% and +3.1%, respectively. Semiconductors were the standout within Tech (up +10.0% and on an 18-day winning streak). Healthcare was the laggard, falling by over 3.0%.

- U.S. Treasury yields edged higher, with the 2-year at 3.78% and the 10-year at 4.30%. The U.S. Dollar Index finished higher, and Gold finished lower. West Texas Intermediate (WTI) crude settled at $94.42, posting a weekly gain of +9.9% as energy supply concerns resurfaced.

- U.S./Iran headlines remained noisy, with a second round of direct talks failing to materialize over the weekend as Iran declined contact with U.S. representatives and President Trump canceled trip by envoys Witkoff and Kushner, leaving the diplomatic path forward uncertain, in our view.

- The Q1 earnings season remained a dominant market force, in our view. The S&P 500 blended earnings per share growth rate rose to just over +15.0%, up from +12.6% at the start of the season, per FactSet, with roughly 82% of reporters beating estimates. Intel posted a standout report on AI-driven CPU demand. Tesla beat estimates, but a sharp increase in 2026 capital expenditure guidance drew scrutiny. UnitedHealth beat and raised. Texas Instruments delivered a strong report led by Data Center and Industrial demand. That said, ServiceNow was the week's notable disappointment, falling sharply on deal slippage tied to the Middle East conflict.

- We believe economic data continues to support a solid fundamental backdrop. March core retail sales rose +0.7% month-over-month, well above the +0.2% consensus estimate, while April flash manufacturing PMI climbed to its highest level since May 2022. Initial jobless claims remained contained, yet the final April University of Michigan consumer sentiment index registered a record low, though inflation expectations ticked modestly lower from the preliminary read.

- Lastly, Kevin Warsh's Fed Chair nomination hearing broke little new ground and was largely dominated by partisan debate. The Justice Department's decision to close its criminal investigation into Chair Powell and to refer the matter to the Fed's Inspector General clears the way for Warsh's Senate Banking Committee vote on Wednesday.

“With indexes near all-time highs and valuations again leaving limited room for disappointment, this week’s unusual convergence of Fed policy signals, Mag Seven earnings reports, key economic data and ongoing geopolitical uncertainty carries significant weight. Notably, investors will be asked to simultaneously assess Fed policy updates, the commercial payoff of AI investments, the durability of economic growth and the inflation risks posed by an unresolved Middle East conflict over the next five days.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

Setting up this week’s “All In Wednesday”

The Federal Reserve’s policy decision on Wednesday sits at the center of a very busy calendar for investors. However, rate policy itself is widely expected to remain unchanged. The CME FedWatch Tool shows that markets are pricing a nearly 100% probability that the FOMC will hold rates steady at the current 3.50% to 3.75% target range. In our view, attention will focus squarely on the policy statement itself and Chair Powell's last press conference. Key questions for investors will likely center on how the Fed characterizes inflation risks tied to energy prices, current labor market trends, and overall financial conditions following sharp equity gains this month. Notably, we believe the statement will reiterate a data-dependent posture, though it could further acknowledge elevated uncertainty surrounding geopolitical developments and their inflation implications, while avoiding any clear signal of near-term changes in the policy path. Bottom line: Investors will spend much of their time post-meeting parsing through the statement looking for small clues on how the committee views the balance of risks at present.

As such, investors will likely be looking for any changes in wording around inflation progress and economic momentum. In our view, markets could be sensitive to whether the Fed explicitly references higher oil prices and, if so, whether those pressures are framed as persistent or temporary. Language around "patience" and "sufficiently restrictive" policy will be closely watched as well. Any refinement in how the Fed describes labor market conditions, particularly wage pressures and hiring demand, could carry implications for expectations around future rate policy. Importantly, the March FOMC vote showed the committee is not fully unified around forward rate policy, as Governor Stephen Miran dissented in favor of a quarter-point cut at the last meeting. Investors will watch whether that dissent broadens this week, as additional dovish or hawkish votes would carry more signal than the unchanged rate itself.

Further, Powell's press conference adds another interesting dimension for investors to watch on Wednesday. With his term as Fed Chair ending on May 15, this week's appearance will be Powell’s final scheduled press conference in that role, assuming Fed Chair nominee Kevin Warsh is confirmed by the Senate on Wednesday. We expect Powell to reiterate continuity in policy decision-making and emphasize that decisions remain driven by incoming data rather than calendar timing. Still, his remarks will inevitably be viewed through the lens of Warsh's sharply different philosophy. In last week’s Senate testimony, Warsh declined to commit to holding press conferences after every FOMC meeting and took direct aim at the dot plot as a mechanism that distorts market expectations. He also argued for fewer officials telegraphing rate decisions in advance. Below the surface, investors may look to see whether Powell's final remarks on Wednesday leave clear guardrails for the Committee as he sees them or open the door to a less predictable communication regime once Warsh takes over.

The Fed meeting this week unfolds alongside a pivotal stretch of Q1 earnings reports, which will be dominated by mega-cap technology. Five of the seven members of the "Magnificent Seven" are scheduled to report results and outlooks this week. If Wednesday’s Fed meeting wasn’t enough to focus on, “All In Wednesday” will also include earnings reports from Alphabet, Amazon, Meta Platforms, and Microsoft. Apple will follow with its report on Thursday, and NVIDIA, the group's most closely watched name for AI infrastructure signals, will report in May. In our view, this week’s five-company cluster of key tech earnings reports will provide the market with a real-time read on whether AI investment is translating into commercial results. The stakes for delivering on investor expectations are unusually high, in our view. According to FactSet, companies beating EPS estimates this reporting season have seen an average two-day stock price increase of +0.9%, in line with the five-year average gain of +1.0%. But with the S&P 500 forward price-to-earnings ratio sitting at 21x, above both its five-year average of 19.9x and its ten-year average of 18.9x, investors are likely to be more guarded in how they reward earnings performance.

Bottom line: Investors are placing a premium on credible earnings guidance, durable revenue streams, and capital discipline, especially as stocks are now back at all-time highs. From our vantage point, Microsoft and Amazon results will be the primary read on cloud demand and enterprise spending conditions. Alphabet and Meta will be central to assessing the momentum of digital advertising and the pace at which AI tools are generating measurable revenue. Amazon's results will likely hinge on AWS growth and whether record capital spending is driving margin expansion. And Apple's report is likely complicated by a CEO transition from Tim Cook to John Ternus, with Services, AI monetization, and tariff risk on hardware as the primary focus items. Across the group, commentary on capital spending plans, cost controls, and forward demand visibility will factor heavily into how markets assess both earnings durability and current valuation levels.

If earnings and policy weren’t enough to focus on, U.S. economic data adds another critical layer to watch. A first look at Q1 GDP, the Employment Cost Index, personal income and spending, and the Fed's preferred inflation gauge for March, the PCE deflator, all land on Thursday. Meaning, following “All In Wednesday”, investors will have less than 24 hours to absorb the Fed's policy machinations and key earnings reports before needing to confront a barrage of growth and inflation data. Earlier in the week, consumer confidence readings and regional manufacturing surveys will provide additional context on demand trends and business sentiment. In total, these economic data points should help inform investor assessments of growth, labor cost pressures, and whether the economic backdrop remains consistent with the Fed's patient policy stance. And finally, overlaying the week’s massive information feed are ongoing tensions in the Middle East. Importantly, the U.S./Iran conflict continues to disrupt shipping traffic in the Strait of Hormuz, and crude oil prices are trading above $90 per barrel. As a result, elevated oil prices are feeding directly into near-term inflation expectations, which, as we are likely to hear this week, are complicating the Fed's price stability mandate. In fact, the Fed's own March minutes noted that rising oil prices have pushed short-term inflation expectations higher, even as longer-term expectations remain relatively stable.

Bottom line: Equities enter the week near all-time highs after rebounding sharply from their March 30 lows. The divergence between equity market optimism and the more cautious signals from bond and oil markets, however, reinforces the view that geopolitical developments remain an active and important variable in risk management. With indexes near all-time highs and valuations again leaving limited room for disappointment (as at the start of the year), this week’s unusual convergence of Fed policy signals, Mag Seven earnings reports, key economic data, and ongoing geopolitical uncertainty carries significant weight. Notably, investors will be asked to simultaneously assess Fed policy updates, the commercial payoff of AI investments, the durability of economic growth and the inflation risks posed by an unresolved Middle East conflict over the next five days. In our view, stock prices already reflect considerable optimism on all these fronts. How the evidence of each stack up this week will likely determine whether the rally can extend or whether the market begins to confront the limits of how far stocks can rise over the near term.

The week ahead:

- Along with the items above, developments in the Strait, oil prices, and Warsh’s Senate Banking Committee vote will be closely watched.