Why the conflict in the Middle East is bigger than just oil

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — MARCH 23, 2026

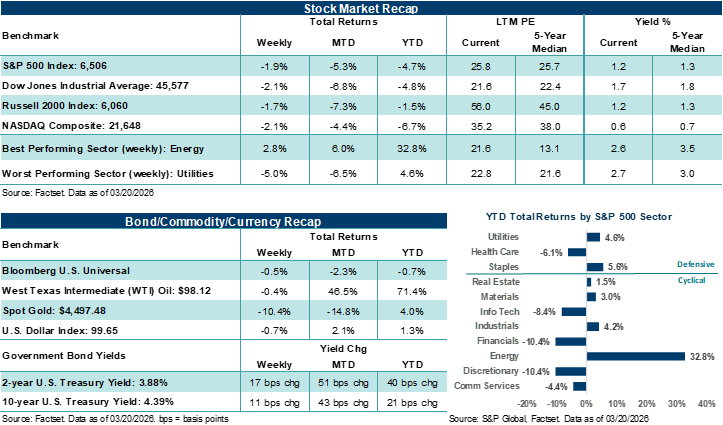

U.S. stocks finished lower for the fourth straight week, as ongoing conflict across the Middle East and strikes on key oil infrastructure kept upward pressure on energy prices. Central banks across the world delivered as expected rate decisions but noted increasing concerns about higher inflation. This week brings a quiet economic calendar, with investors' focus remaining locked on Middle East developments and quarter-end positioning.

Last week in review:

- Major U.S. stock averages closed the week lower by roughtly 2.0%

- U.S. Treasury yields moved higher. The U.S. Dollar Index moved lower. Gold posted its worst week since 2011.

- West Texas Intermediate (WTI) oil ended essentially flat, though Brent crude pushed higher by nearly +9.0%.

- The Federal Reserve left its rate policy unchanged. However, the committee raised its inflation targets and growth forecasts for this year and pushed back against expectations for near-term rate cuts given current inflation dynamics.

- February producer inflation came in hotter than expected, while pending home sales posted a surprise gain and new home sales fell to their lowest level since October 2022. Jobless claims remained muted.

- By the numbers: $1 trillion plus in datacenter revenue orders through 2027 seen by NVIDIA; 33.3% is the increase in the average national price of a gallon of gasoline over the last month (AAA); 13 is the number of consecutive weeks the Energy sector has posted a gain.

“Investors should be prepared for continued volatility. Whether that comes from traders searching for new technical levels in the market or near-term fundamental conditions across the global economy evolving due to conflict in the Middle East. But regardless of the near-term direction of stocks, we remain confident that equities will eventually work through this difficult period, especially if fundamental conditions don’t buckle under global stress. As most investors know, stocks have a long history of weathering unexpected shocks and dislocations. Nevertheless, it’s sometimes helpful to remind ourselves of this point when conditions don’t feel so certain.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

Why the conflict in the Middle East is bigger than just oil

As the first quarter winds down, major U.S. stock averages are on pace for losses, which likely comes as no surprise to anyone. Although the quarter isn’t over yet, weaker momentum in Big Tech, AI disruption fears, elevated energy prices, and growing anxiety about the growth outlook are weighing on investor sentiment. That said, President Trump, in a Truth Social Post, appears to be opening a door for de-escalation in the conflict in Iran, which could see asset prices rebound if conflict soon subsides. That said, we thought we would highlight one item that adds to the list of investor worries and one that offers a longer-term “positive” perspective amid a growing set of concerns.

In an item that piles on the negative vibes, as the Iran conflict drags on, investors are considering global economic impacts beyond the current energy shock. While the well-documented risks to crude oil and liquid natural gas that flows through the Strait of Hormuz have caused prices to spike, it’s important to note that the Middle East is also a major supplier of industrial and agricultural commodities deeply embedded in global supply chains. According to the Center on Global Energy Policy at Columbia University SIPA, the Persian Gulf produces globally significant levels of commodities such as urea (45%), helium (39%), methanol (35%), ammonia (30%), sulfur (22%), aluminum, polyethylene, and polypropylene. These commodities support activities ranging from fertilizer production and semiconductor manufacturing to packaging, automotive manufacturing, construction materials, and medical imaging. And as Barron’s recently noted, the Iran conflict and the effective closure of the Strait of Hormuz are starting to pressure parts of the global economy that are not immediately associated with oil. For example, fertilizer prices are rising into the spring planting season, helium shortages are becoming a growing concern for semiconductor production in Asia, and aluminum exports from the Gulf are becoming harder to move. Bottom line: We believe global economic risks are rising as basic materials and chemical inputs that support food production, electronics, manufacturing, and health care experience increasing supply chain disruptions due to the conflict in Iran. It’s a growing issue that has been overshadowed by the larger headlines regarding higher oil, gas, and LNG prices, but may start to attract more attention if the conflict wears on.

Notably, these pressures could create supply chain problems outside the Middle East. In our view, Asian economies are especially exposed because of their dependence on Gulf energy and industrial inputs, but the fallout is also affecting American farmers and European drugmakers, according to insights from Barron’s. For instance, U.S. farmers are quickly seeing pressure from higher diesel and fertilizer costs, which could raise the risk of weaker crop yields and higher food prices here at home. In addition, semiconductor producers in South Korea and Taiwan could face intermediate-term helium constraints, potentially squeezing the global electronics supply chain. And in Europe, pharmaceutical logistics are becoming more complicated as drug shipments that normally pass through Gulf cold-chain hubs are rerouted. Bottom line: If conflict persists, global growth is likely to come in lower than most have forecast for at least the first half of the year as input and supply pressures widen beyond oil and fuel. Unfortunately, this could feed broader inflationary pressures through food, manufacturing, and medical supply channels, while reinforcing the need for more diversified sourcing and transportation networks in the longer term, especially across Asia and Europe. These dynamics harken back to the early days of the COVID-19 pandemic, in our view.

Importantly, following last week’s Federal Reserve, European Central Bank, Bank of England, and Bank of Japan meetings, the world’s largest central banks all communicated a very similar message. Each is watching inflation pressures very closely and monitoring evolving conditions in the Middle East, and if the situation becomes more impactful for inflation or growth, they stand ready to adjust policy. However, for now, central bank messages are leaning toward a more hawkish stance, in our view, as each wants to show it’s attentive to rising inflation pressures, which means rate cuts without a larger deterioration in growth are likely to stand off to the side for now.

Some historical perspective on recent stock stress

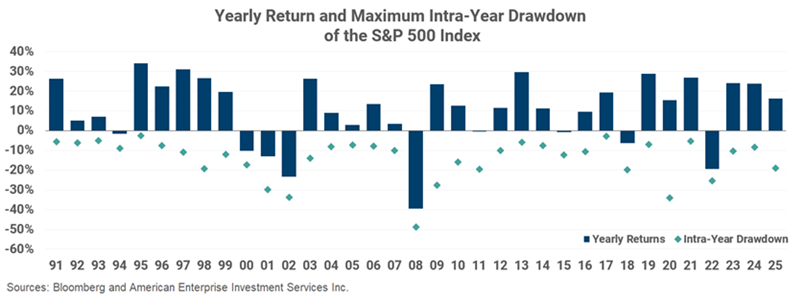

Closer to home, we decided to devote a little space this week to drawing investors' attention back to the longer term. Interestingly, the S&P 500 broke below its 200-day moving average last week for the first time in over a year. The threshold represents the longer-term trend line in stock direction, which has been sloping higher for several months. Importantly, despite sideways trading and periods of market stress over recent months, the S&P 500 remained firmly above its longer-term trend line, which helps add confidence that well-entrenched trading dynamics remain firm. But larger price declines in the Index as of late, driven by AI disruption and private-market fears as well as rising anxiety over conflict in the Middle East, have now pushed the U.S. stock barometer below all its key trading levels. Thus, with the Index finally breaking below the 200-day moving average last week, traders may become concerned that a more negative near-term shift in stock direction could occur. That said, other technical indicators suggest that stocks may be approaching “oversold” territory, which historically provides solid longer-term buying signals for traders and investors, at least eventually. President Trump’s Truth Social Post indicating substantive talks with Iran are underway could provide a positive catalyst for near-term stock momentum. Bottom line: That said, investors should be prepared for continued volatility. Whether that comes from traders searching for new technical levels in the market or near-term fundamental conditions across the global economy evolving due to conflict in the Middle East. But regardless of the near-term direction of stocks, we remain confident that equities will eventually work through this difficult period, especially if fundamental conditions don’t buckle under global stress. As most investors know, stocks have a long history of weathering unexpected shocks and dislocations. Nevertheless, it’s sometimes helpful to remind ourselves of this point when conditions don’t feel so certain.

Finally, it can also be helpful to frame the uncertainty of the day and recent negative stock reactions within a historical context. As the chart below shows, throughout history, the S&P 500 can tumble lower during certain points in any given year but not always finish the year lower (2025 being the most recent example). And while yes, there’s a risk this year could turn out not so pleasant for investors if fundamental conditions worsen due to some of the concerns of the day, history is littered with examples of positive annual finishes for the S&P 500 and intra-year declines much more aggressive than those experienced thus far. Something to keep in mind if the days ahead remain challenging to navigate.

The week ahead:

- Preliminary looks at March S&P Global manufacturing and services activity will be released on Tuesday.

- January consumer spending, February import/export prices, and weekly jobless claims will be other points of interest.