Markets head into the summer with the bulls and bears increasingly at odds about the next move

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — MAY 26, 2026

The S&P 500 Index advanced higher for the eighth straight week, despite increasing pressures from rising interest rates and elevated oil prices. NVIDIA again wowed investors with its earnings results, but the stock finished last week lower. This week, the Federal Reserve’s key inflation data is on deck, and it’s likely headed higher.

Last week in review:

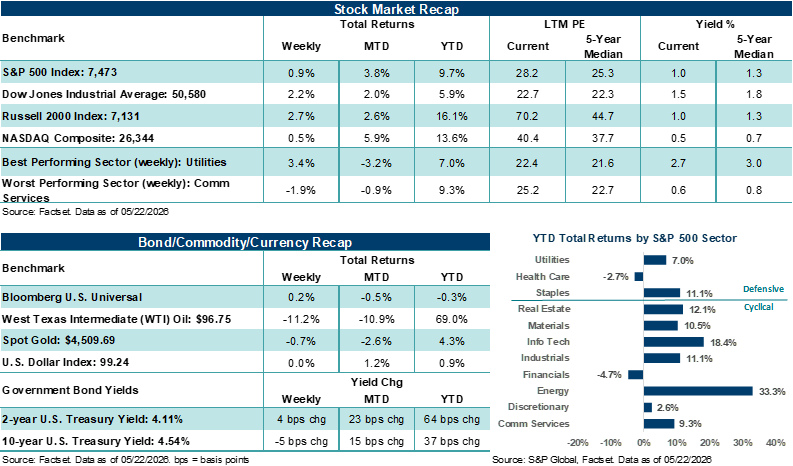

- The S&P 500 advanced +0.9% and is on pace for its second straight month of gains. All major U.S. stock averages finished the week higher, led by a gain of +2.7% in the Russell 2000 Index.

- U.S. Treasury prices finished mostly firmer. However, attention intensified on rising yields across the 10-year and 30-year as of late, helping push back on stock momentum. Gold finished lower, the U.S. Dollar Index ended little changed, and West Texas Intermediate (WTI) crude fell on optimism around U.S./Iran diplomacy headlines.

- Final May University of Michigan consumer sentiment fell to a record low amid higher cost-of-living concerns, weekly jobless claims remain subdued, and preliminary May data on manufacturing and services activity showed expansionary conditions.

- SpaceX filed for its IPO (likely set for next month) and Kevin Warsh was sworn in as Fed Chair.

“The market is entering the summer months with a clear push-and-pull dynamic that could expose investors to bouts of volatility. AI-driven growth and a still-stable consumer could provide notable support for stocks at a broad level, but higher bond yields and sticky inflation are growing concerns that may cap upside if these conditions persist.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

Markets head into the summer with the bulls and bears increasingly at odds about the next move

As we return from the Memorial Day holiday and begin the unofficial start of summer, investors face both supportive growth narratives that could benefit stocks over the coming months as well as a growing set of macroeconomic headwinds that will likely need careful monitoring, especially as stocks sit near all-time highs.

At the highest level, we believe the AI buildout story continues to anchor the upside narrative across major averages, with NVIDIA's earnings report last week helping reinforce that view (more on that below). However, as important as NVIDIA is to overall market sentiment, we see the AI story becoming more inclusive of additional sub-trends. For example, Anthropic is on track for another sharp step-up in revenue, OpenAI highlighted progress on reasoning models, and infrastructure and energy tie-ins to AI growth continue to expand.

On the economic front, the consumer (responsible for 70% of U.S. GDP) remains more stable than some might have expected after oil prices jumped following the Iran conflict. For example, off-price and home improvement retailers cited steady demand in their earnings reports last week. At the same time, payment data and higher-level economic indicators (such as retail sales) continue to reflect healthy underlying spending, supported by still-low U.S. unemployment.

And geopolitics, while still a key risk factor for market momentum, has shifted in a more constructive direction. We believe ongoing diplomatic dialogue between the U.S. and Iran has reduced the risk of a near-term escalation in violence, and activity through the Strait of Hormuz is showing small signs of progress, something that has been lacking for some time now. Against a backdrop of exceptionally strong Q1 earnings growth, forecasts of continued strong earnings growth over the next few quarters and a still-expanding U.S. economy, we believe there are clear reasons for the bulls to remain cautiously positive on the outlook for stocks over the coming months.

But it’s not all sunshine and rainbows out there, especially in the bond market, which has become a growing source of concern for the bears. The sharp backup in Treasury yields over recent weeks is drawing increased attention, with the long end of the curve reaching levels not seen since before the Global Financial Crisis. Yet, more important than the move in rates is the growing concern around its drivers. Building inflation pressures, deteriorating fiscal dynamics, and ongoing geopolitical risks are increasingly being viewed as persistent problems that, if they become entrenched, could keep interest rates elevated. And as seen more aggressively last week, the correlation between stocks and bond yields has turned sharply negative, meaning higher rates are acting as a direct headwind to stocks and valuations. Historical patterns suggest that sustained bond market weakness, and higher yields as a result, has typically required either an economic slowdown or market stress to reverse. Either way, recent bond developments are not a great setup for stock prices heading into the summer.

In addition, recent economic data is also adding to the bear’s anxiety. May's preliminary PMI readings last week, while still expansionary (a bullish factor), pointed to renewed cost pressures, with both input and selling prices rising (a bearish signal). Importantly, some of the manufacturing strength appears tied to business stockpiling ahead of potential disruptions.

Interestingly, FOMC minutes from the last Fed meeting reinforced a cautious tone among policymakers, with a majority of the committee signaling a willingness to tighten rates further if inflation pressures remain above target. As a result, market odds suggest the Fed is likely to hold or “raise” rates by year's end. Thirty days ago, odds pointed to a hold or “cut” in policy rates by year’s end. Given the changing tone on rates, we expect markets to test newly minted Fed Chair Kevin Warsh over the coming months to get better insight into his leadership style and ability to steer monetary policy with inflation above target.

More directly tied to stocks, positioning and sentiment are also worth watching as we move into the summer months. Survey data suggests investors are leaning more aggressively into equities, which could trigger short-term contrarian signals. At the same time, hedge fund positioning shows elevated short exposure, which raises the risk of sharper countertrend moves that could increase equity volatility should markets move against these types of investors.

Finally, on the headwinds front, even broadly solid profit results across retail and industrials last week were met with selling pressure when guidance or commentary introduced uncertainty. Simply, investor expectations are elevated after the market's run since the March lows, and at current levels, investors might now be less willing to look through near-term risks.

Bottom line: The market is entering the summer months with a clear push-and-pull dynamic that could expose investors to bouts of volatility. AI-driven growth and a still-stable consumer could provide notable support for stocks at a broad level, but higher bond yields and sticky inflation are growing concerns that may cap upside if these conditions persist. In our view, the direction of the market’s travel from here could hinge on whether rates stabilize and whether incoming economic data confirms that growth can hold without reigniting inflation.

Closing the loop on NVIDIA: Last week, we outlined several items investors needed to see in NVIDIA's profit report, including another step higher in guidance, confirmation that inference demand is building, updates on next-generation chips, margin durability, clarity on China, and evidence that the company's competitive position remains intact. In our view, the report checked those boxes with hard-to-wash-out ink. Revenue has now grown from roughly $44 billion to over $81 billion in just one year, marking the third consecutive quarter of annual acceleration. Data Center revenue nearly doubled. Gross margins stabilized around 75%. And forward guidance of $91 billion for the fiscal second quarter came in well above the roughly $87 billion consensus, continuing the pattern of guiding higher and then beating. The company also increased capital returns, raising its quarterly dividend to $0.25 per share from $0.01 and authorizing an additional $80 billion in share repurchases. Notably, management highlighted the Vera Rubin platform, including the Vera CPU, which opens a market the company has never participated in before. In our view, one of the most important reports of the earnings season confirmed that AI demand is broadening, the product cycle is deepening, and NVIDIA's position at the center of the buildout remains integral.

The stock, however, slipped following the report, marking its fourth consecutive post-earnings decline, and ended the week lower by 4.5%. Of course, the law of large numbers and expectations around the company might be beginning to catch up with the stock. But we also believe the macroeconomic backdrop, which has been looking more mixed as of late, could be weighing on growth stocks after an already strong run from the March lows. And while NVIDIA's fundamentals gave investors little to push back on, higher rates are beginning to test what investors are willing to pay for growth, even when the earnings story is as strong as NVIDIA’s.

We also flagged the widening gap between semiconductor strength and software weakness as a dynamic to watch. NVIDIA's commentary around agentic AI, real-world inference demand, and enterprise adoption suggests the conditions for that gap to narrow may be forming, but it has yet to show up in software stock performance. We’ll see how that performance gap develops over the coming month before the next earnings season starts in July.

Bottom line: NVIDIA’s report last week further advanced the AI thesis and the growing ecosystem that could keep broader averages heading higher this summer, albeit with potentially more volatility. Yet, the larger near-term question heading into the summer is whether the rate and inflation backdrop will sour some of the enthusiasm for AI now that the Q1 earnings season is essentially in the rearview mirror. Long story short, the typical summer doldrums may be anything but this year.

The week ahead:

- Thursday’s April Personal Consumption Expenditures (PCE) Price Index should confirm what other inflation data have already shown this month. That is, higher oil prices are feeding into the U.S. economy and raising the risk of a slowdown.

- May consumer confidence should show another step down in sentiment as higher fuel prices erode purchasing power.

- Profit reports from AutoZone, Salesforce, Costco, and Dollar Tree will help start to put a cap on the Q1 earnings season.