The state of AI ahead of NVIDIA’s earnings report this week

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — MAY 18, 2026

The S&P 500 Index eked out a seventh consecutive weekly gain, while the NASDAQ Composite snapped its six-week winning streak. Investors navigated higher Treasury yields, firmer inflation data and another round of artificial intelligence-related headlines. This week, NVIDIA’s earnings report will take center stage, while a heavy slate of retail profit reports will help shed more light on the state of the consumer amid gasoline prices above $4.50 per gallon.

Last week in review:

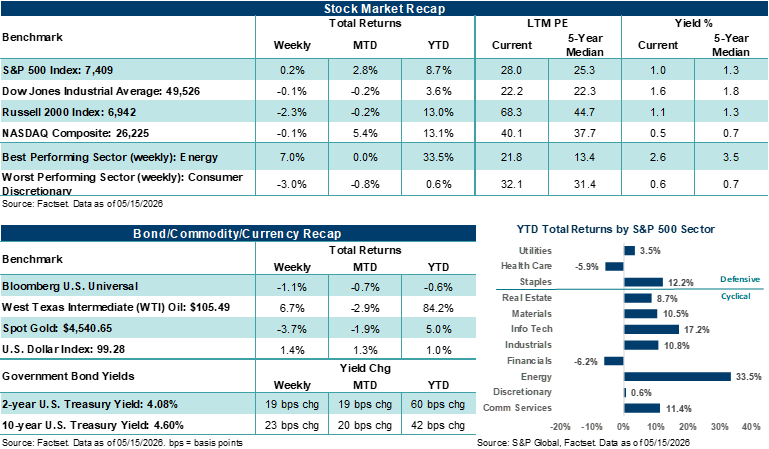

- The S&P 500 Index gained +0.1% last week. The Dow Jones Industrial Average slipped 0.2%, the NASDAQ Composite declined 0.1%, and the Russell 2000 Index fell 2.3%. Energy led all S&P 500 sectors as crude prices rose sharply, while Consumer Discretionary lagged, ahead of key earnings reports this week.

- U.S. Treasury prices weakened last week, with the 30-year yield moving above 5.0%, touching its highest level since July 2007. The U.S. Dollar Index rose, Gold fell, and West Texas Intermediate (WTI) crude gained +6.7%.

- On the economic front, April core CPI and core PPI topped expectations largely due to higher energy prices. And April retail sales came in largely in line but slowed from March’s stronger pace.

- Finally, geopolitical headlines remained active last week as uncertainty around Iran and the Strait of Hormuz increased. Notably, the Trump-Xi summit somewhat underwhelmed expectations, with no major breakthroughs in the Iran conflict.

“The AI infrastructure buildout is expanding. The capital commitments are historic. Earnings strength is confirming demand, and the cycle is broadening from chips into memory, networking, power and system design. These are all positives for the current state of AI. But valuations across the hardware complex largely reflect a market that has already priced in a lot of the good news.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

The state of AI ahead of NVIDIA’s earnings report this week

Last week, markets hit a series of milestones. The Dow again briefly touched 50,000. The S&P 500 Index crossed 7,500. NVIDIA reached a new all-time high. And Cerebras, an AI chipmaker most investors haven’t heard of, went public, ending the week with a valuation of roughly $60 billion. But by Friday, the vibes were shifting. The 10-year Treasury yield climbed to 4.60% (the highest since February 2025), oil rose on Middle East concerns, and the stock rally finished the week on a softer note, particularly within Technology. So, while the AI rally has gained momentum over recent weeks, investors were reminded that the broader market backdrop can quickly become less supportive. NVIDIA’s earnings report on Wednesday may help set the tone for where the AI trade and the broader market go from here.

In our view, the positive investment case for AI starts with the nearly three-quarters of a trillion dollars in combined 2026 capital spending commitments from Amazon, Microsoft, Alphabet and Meta Platforms. These are the largest single-year corporate capital expenditures in history, and early returns suggest the spending is already producing results. Azure cloud growth reached 40% in the latest quarter. Microsoft’s AI business is now generating revenue at an annual run rate of $37 billion. Anthropic, the private AI company behind Claude, has grown quickly enough that it recently leased an entire data center and its 220,000-plus NVIDIA GPUs because internal capacity couldn’t keep up. And NVIDIA CEO Jensen Huang said in March the company’s pipeline for current and next-generation chips now stands at $1 trillion through 2027, double what he projected a year ago.

Importantly, AI demand is also showing up across a broader set of companies. Recent earnings reports from semiconductor, memory, networking and infrastructure companies have pointed to continued AI-related strength. For example, Cisco raised its AI order target for the year by roughly 80% to $9 billion. Taiwan Semiconductor Manufacturing lifted its long-term semiconductor market forecast to $1.5 trillion by 2030. SK Hynix, the South Korean memory chipmaker, is approaching a $1 trillion market cap after selling out its 2026 supply of advanced memory chips used in AI systems. And the Philadelphia Semiconductor Index (SOX) hit an all-time high last week, up over +62% from late March.

The AI trade is widening as well. As mentioned above, Cerebras went public last week in the largest AI initial public offering (IPO) ever, and the deal was heavily oversubscribed. The company makes a unique type of AI chip designed for “inference”, or the process of running AI models after they have already been trained. Inference is increasingly important because every chatbot response, search result and AI agent completing a task requires computing power. In our view, the fact that investors have ascribed such a valuation to a company built around this part of the AI ecosystem suggests the market believes AI usage, not just AI training, could become a major source of future demand.

Software, however, has been left behind. The iShares Expanded Tech-Software Sector ETF (IGV) is down roughly 13% year-to-date, while the VanEck Semiconductor ETF (SMH) is up roughly +54%. As of last week, that gap was the widest on record. Some of that pressure began in February, when Anthropic released AI workplace tools that could automate tasks such as contract review, compliance checks and sales preparation. Those functions sit at the heart of what many existing software companies provide today. If AI can do the work, do companies still need as much software? The answer is complicated. Investors have since walked back some of their worst-case fears, and companies tied to cloud infrastructure, data, cybersecurity and AI adoption have continued to post solid results. However, we believe the market is drawing a clear line between companies that rely heavily on traditional per-seat subscriptions and those positioned closer to the center of the AI buildout.

So, what does NVIDIA’s report need to show this week? Outside of the previous quarter’s results, which most investors expect to be strong, we believe the following items will be top of mind.

- Q2 revenue guidance. NVIDIA has guided higher in each of the last three quarters, only to ultimately beat estimates. That pattern has become the expectation. Anything less than another step higher in guidance would likely disappoint.

- Inference demand. The AI bull case has evolved from training larger models to supporting the growing volume of real-world AI usage. Investors will want to hear that NVIDIA’s chips remain well positioned for the next phase of demand.

- Next-generation chips. NVIDIA’s Vera Rubin platform is now expected to begin shipping in July, seven months ahead of schedule. Any update on customer demand or the production ramp could shape expectations for the rest of the year.

- Margins. Gross profit margins expanded throughout last year, reaching 75% in the most recent quarter. The question is whether that level can hold as component costs rise and new chip transitions add complexity. A potential Samsung strike on May 21 could add a near-term wrinkle because Samsung is one of only three companies that produce the advanced memory chips NVIDIA’s systems require.

- China. The Trump-Xi summit ended last week with the U.S. clearing the way for some Chinese companies to buy NVIDIA’s H200 chips. NVIDIA’s guidance already assumes no revenue from China’s data center market, so any positive change or commentary could be seen as future upside and supportive of the current stock price.

- Competition. Broadcom is building custom chips for hyperscalers. Cerebras is offering a different architecture for inference. And AMD’s accelerator business is growing. However, NVIDIA still holds the strongest position. Investors will want confirmation that its industry lead remains intact.

More broadly, NVIDIA now represents 8.6% of the S&P 500, with a market capitalization of $5.5 trillion. A strong report with strong forward guidance would likely reinforce the AI trade and support the semiconductor companies that have rallied alongside it – likely a positive for the broader market. Conversely, a softer result or outlook could ripple across the sector and the broader market, especially given how much good news appears to be reflected in AI-related chip stocks today.

And as investors were reminded on Friday, the macro environment still matters. The 10-year Treasury yield sits at its highest level in over a year. April producer inflation came in at its hottest level since December 2022, and consumer inflation continues to rise. In our view, higher bond yields and firmer inflation could start to challenge what investors are willing to pay for long-duration growth stories, even when the underlying fundamentals remain strong. Further, Goldman Sachs recently noted that hyperscaler capital spending is absorbing the vast majority of operating cash flows, leaving less room for share buybacks, which have historically supported earnings growth at the Index level.

Outside the obvious focus points from NVIDIA’s report this week, is whether the company can begin to narrow the gap between semiconductor strength and software weakness. If AI usage is truly moving from model training into real-world applications, agents and enterprise tools, that should eventually benefit the software companies building on top of the infrastructure. Anthropic’s rapid growth is early evidence that the dynamic is taking shape. The question is whether the rest of the software industry follows, and how quickly the hardware buildout can set the foundation for software to do what it has historically done well, which is building applications that improve how consumers and businesses interact with the world.

Bottom line: The AI infrastructure buildout is expanding. The capital commitments are historic. Earnings strength is confirming demand, and the cycle is broadening from chips into memory, networking, power and system design. These are all positives for the current state of AI. But valuations across the hardware complex largely reflect a market that has already priced in a lot of the good news. Simply, NVIDIA's report on Wednesday must show that demand is still growing fast enough to justify what the market has already priced in to keep the momentum up. However, it may have to do so as investors become increasingly concerned about elevated interest rates and commodity prices, as well as ongoing disruptions in the Middle East.

The week ahead:

- Along with NVIDIA, Home Depot, Target, Lowe’s, TJX, Walmart, and Ross Stores will report their latest profit results.

- On the economic front, home data, the latest FOMC Minutes, and May preliminary looks at manufacturing and services activity line the week.