SpaceX is set to make history this week: Why perspective over access matters most to investors

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — JUNE 8, 2026

The S&P 500 Index's nine-week winning streak came to an end last week, as a stronger-than-expected May jobs report and a sharp selloff in semiconductors triggered the broadest risk-off session in over a year. This week, May CPI and PPI data, Apple's Worldwide Developers Conference, the SpaceX IPO, and $119 billion in Treasury auctions will be in focus.

Last week in review:

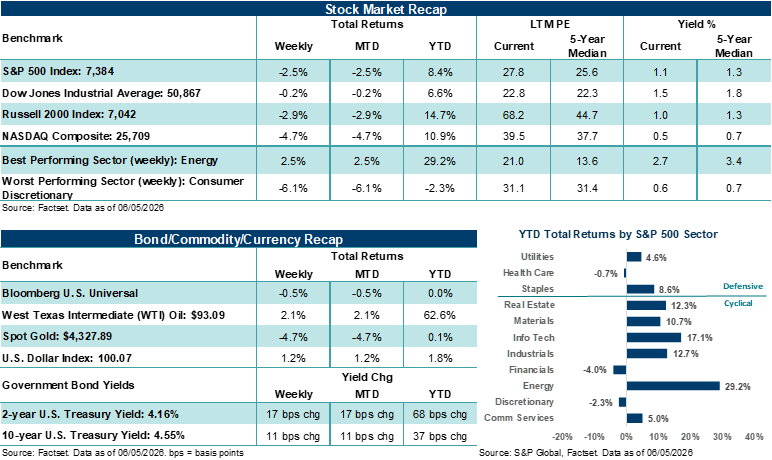

- The S&P 500 Index fell 2.5% last week, while the NASDAQ Composite dropped 4.7%, its worst week since the April 2025 Liberation Day selloff. The Dow Jones Industrial Average slipped 0.2%, and the Russell 2000 Index declined 2.9%.

- The week's defining move was a sharp selloff in semiconductors and AI-related stocks. Broadcom beat on earnings, but its AI chip revenue guidance fell short of elevated expectations, triggering a sell-the-news reaction across the chip complex as well as Information Technology more broadly. The Philadelphia Semiconductor Index fell by over 10% on Friday and 4.7% on the week. That said, the chip index is still up an astonishing +71% since the March lows.

- Treasury prices weakened, as the rise in yields accelerated after Friday's jobs data. The U.S. Dollar Index moved higher. Gold fell 5.0%, and Bitcoin lost nearly 17% for its worst week since November 2022. West Texas Intermediate (WTI) crude rose +2.1% for the week despite Friday's decline.

- Notably, labor market data came in stronger than expected. May nonfarm payrolls rose +172,000, well above the roughly 88,000 Bloomberg estimate. March and April jobs were revised higher by a combined +93,000. The unemployment rate held steady at 4.3%, and average hourly earnings rose +0.3% month over month. The three-month payroll average is now the highest since March 2024. Separately, May ISM manufacturing and services activity also came in better than expected.

- Geopolitical progress on Iran stalled. Despite hopes earlier in the week that a 60-day memorandum of understanding was close, the U.S. conducted additional strikes in southern Iran while Gulf nations responded to inbound attacks from Iran. Expectations still lean toward a negotiated settlement, but we believe key sticking points around nuclear material, the Strait of Hormuz and sanctions relief remain unresolved and could put upward pressure on oil prices this summer.

- Finally, Friday's selloff was driven by two colliding forces, in our view. First, a hotter jobs report that pushed Fed rate-hike expectations higher, and second, two days of aggressive selling across the semiconductor space. Importantly, the rotation into Consumer Staples, Utilities, and Healthcare on Friday suggests investors aren't leaving the market. They're repositioning within it. Economic and corporate fundamentals enter this potential period of recalibration from a position of strength, following nine consecutive weeks of gains. A few clouds on the horizon, or even the occasional rain shower, shouldn't rattle investors after such a long stretch of nearly uninterrupted sunshine.

“SpaceX, Anthropic, and OpenAI likely represent real long-term opportunities for those patient and tolerant enough to contend with what could be several periods of volatility over the coming quarters and years.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

SpaceX is set to make history this week. Why perspective over access matters most to investors.

SpaceX is expected to go public this week and, by all accounts, will take the top spot for becoming the largest initial public offering (IPO) in history. The company plans to price its shares at $135, raising roughly $75 billion at a valuation near $1.75 trillion. Pricing is expected on June 11 and trading on the Nasdaq under ticker SPCX on June 12. At its launch, SpaceX will become the seventh-largest public company in the U.S. on day one and put the raise well ahead of the current global IPO records set by Saudi Aramco’s $29.4 billion offering in 2019 and Alibaba’s $25 billion U.S. listing in 2014. And given CEO Elon Musk’s propensity to defy convention, the deal's structure is unique as well. Rather than use a traditional price range to gauge demand for an IPO, SpaceX is marketing the offering at a fixed price. And for a deal of this size, that’s likely a clear signal of confidence in investor appetite, in our view.

Notably, SpaceX is unlikely to be the only high-profile deal investors will need to absorb this year. Anthropic has already filed for an IPO, and OpenAI is widely expected to follow, which means 2026 could see a wave of mega-cap AI and AI-related supply hitting public markets. Thus, the IPO market is heating up and, unlike years past, may include three unusually large IPOs all competing for investor dollars.

What could this trio of mega-cap IPOs mean for the rest of the market? On the institutional side, the setup looks fairly straightforward. Large mutual funds and index-linked strategies typically raise cash ahead of offerings like this and, in many cases, fund participation by trimming existing positions. At the scale of SpaceX, Anthropic, and OpenAI, that likely means reallocating capital away from areas of the market that have already performed well, particularly large-cap growth and AI-linked names. As such, when new equity supply enters the market at this magnitude, it most likely needs to be funded through existing holdings, at least across managed, indexed, and institutional strategies.

However, the retail side of the demand equation is less clear, in our view. For one, there’s still a large amount of cash sitting in money market funds, including $7.9 trillion in total assets, according to Investment Company Institute data. That represents a meaningful pool of sidelined capital that could move into equities, and forthcoming IPOs, if investor interest proves strong. Retail participation in SpaceX is also expected to play a larger role than what is typical in new offerings and could play a role in Anthropic and OpenAI’s launch if SpaceX’s debut is successful. So, while institutional investors may be redirecting capital to participate, there is at least a credible case that some portion of demand could come from new, rather than recycled, funds on the retail side.

That said, it’s not unreasonable to anticipate that the market could move through a period of rotation, funding shifts, and potentially some lost momentum in the same parts of the market that have benefited most from the AI trade. In our view, these IPOs are competing for the same dollars already committed to AI leadership. If capital needs to be freed up, the pressure is unlikely to be evenly distributed. And we believe that potential pressure is more likely to appear first in some of the most crowded positions. Last week’s softer trading in semiconductors and AI-related stocks may already echo this dynamic.

In particular, for SpaceX, the valuation case also raises the bar for what has to go right once it’s a public company and more investors can assess its fundamentals over time. According to projections from Goldman Sachs, an underwriter in the IPO, SpaceX’s total revenue could grow from $18.7 billion in 2025 to roughly $474 billion by 2030, with its AI segment expected to expand from about $3.2 billion to approximately $322 billion over the same period. That implies a near-100-fold increase in AI-related revenue and suggests the IPO is being driven less by the current business mix and more by expectations that SpaceX will emerge as a meaningful player in the AI ecosystem over the next several years.

By almost any reasonable metric, that’s a bold assumption. Goldman’s projections imply not just growth, but competitive success in an area already led by companies like OpenAI, Anthropic, and Alphabet. At the same time, independent estimates, such as from Morningstar, have placed SpaceX’s valuation closer to $780 billion, well below the proposed IPO level. In our view, that gap highlights the extent to which the IPO is pricing in future outcomes that remain uncertain.

History adds another layer of perspective and complexity for investors to navigate. Recently, Truist analyzed the 30 major IPOs over the last 15 years and found that the average company experienced a maximum drawdown of roughly 55% in its first year of trading, even when the underlying businesses were well known. Median returns in that group were weak at both the six-month and 12-month marks. Further, data from Bespoke Investment Group points in a similar direction. Looking at the three largest IPOs in each year since 1998, the pattern is clear. Returns tend to be strongest early after an IPO launch, but performance often softens over time, particularly around the six-month window when lockups expire, and additional supply enters the market. Note to investors: Strong IPO debuts don’t always translate into smooth follow-through over the next year, as earnings reports and more fundamental data become available to trade against.

Bottom line: SpaceX, Anthropic, and OpenAI likely represent real long-term opportunities for those patient and tolerant enough to contend with what could be several periods of volatility over the coming quarters and years. SpaceX sits at the intersection of launch infrastructure, satellite communications, AI and defense technology. Anthropic and OpenAI are central to the development of large language models and the next phase of AI applications. But compelling stories don’t automatically create favorable entry points or revenue that matches the size and scale of these private companies, which will soon step into the public light. Importantly, these businesses are becoming, or are expected to become, public at a time of high expectations, rapidly evolving technological change, and operating models that are still being tested at scale, not only within tech but also across industries.

For SpaceX specifically, a $1.75 trillion valuation, supported by projections that call for nearly 100x growth in AI alone, leaves little room for missteps, in our view. For investors who choose to participate, sizing matters (i.e., keep positions small to start). Time horizon matters (think in years and decades). And the willingness to look through potential periods of volatility matters a great deal (expect drawdowns from time to time, maybe large). Let’s also keep in mind that these companies are not mature business models entering public markets at conservative valuations. They are high-expectation companies entering a public setting for the first time in areas that are still taking shape and in their infancy. The opportunity is exciting, and the long-term growth potential may be underappreciated with a long enough time horizon. But so is the risk that it takes longer for these stocks to find their footing than current valuations suggest, particularly as the market works through how to truly evaluate these companies and the emerging industries they operate in.

The week ahead:

- May CPI on Wednesday and PPI on Thursday will be the key economic releases, offering the next read on whether inflation pressures are easing enough to keep the Fed on hold.

- The Fed enters its blackout period ahead of next week’s FOMC meeting, with no scheduled speakers this week.