The Supreme Court strikes down IEEPA tariffs. And the market braces for NVIDIA's earnings update

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — February 23, 2026

Major U.S. stock averages finished higher last week, with the S&P 500 Index back in the green for the year. However, last week’s Supreme Court decision to strike down President Trump’s reciprocal tariffs likely complicates the trade environment from here, while NVIDIA’s earnings report this week could play a significant role in how major averages trade over the near term.

Last week in review:

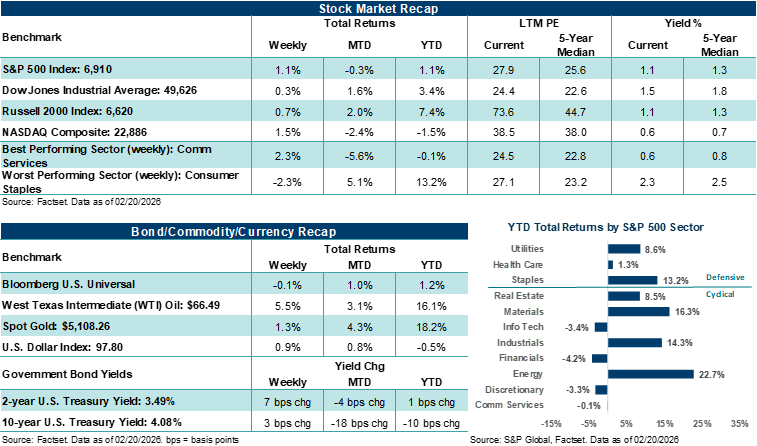

- The S&P 500 Index gained +1.1%, while the NASDAQ Composite advanced +1.5%. The Dow Jones Industrial Average and Russell 2000 Index rose +0.3% and +0.7%, respectively.

- U.S. Treasuries finished mixed, the U.S. Dollar Index moved higher, Gold settled higher, and West Texas Intermediate (WTI) crude jumped +5.5% on rising U.S./Iran tensions.

- Q4 U.S. GDP rose just +1.4%, much weaker than the +4.4% pace seen in Q3. The weaker growth was largely attributable to the government shutdown, while consumer and business spending in the prior quarter remained solid.

- December core PCE inflation, the Fed’s preferred measure, came in hotter than expected (+3.0% annualized) due to rising goods prices (partly a function of tariffs), and remains well above the Fed’s +2.0% target.

- Preliminary looks at February manufacturing and services activity showed both measures remained in expansion, though U.S. business activity grew at its slowest pace in ten months.

- The U.S. Supreme Court ruled that President Trump’s reciprocal tariffs were unlawful.

“Since the end of last year, Technology trade, particularly around artificial intelligence, has shifted from ‘show me the promise’ to ‘show me the money’.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

The Supreme Court strikes down President Trump's IEEPA tariffs

On Friday, the Supreme Court ruled that President Trump’s use of the International Emergency Economic Powers Act (IEEPA) to enact sweeping tariffs across the world starting last April was unlawful. Simply, the Court said the emergency law does not give the President authority to impose reciprocal tariffs, nor does it authorize the IEEPA duties tied to his fentanyl and border emergency actions. U.S. Customs and Border Protection previously reported that $133.5 billion had been collected under IEEPA as of mid-December 2025, accounting for about 67% of the tariffs collected in fiscal year 2025. However, the Court offered no direction on how companies will be reimbursed for these tariffs. Notably, the Supreme Court ruling does not unwind tariffs imposed under other statutes, including Section 232 and Section 301 programs, leaving about 40% of all existing tariffs in place, including on steel, aluminum, autos/parts, solar panels, and some China-related goods.

The White House’s response was swift and immediate. Trump announced a new 15% global tariff under Section 122 of the Trade Act of 1974, in addition to existing duties. However, unlike IEEPA, Section 122 has limitations. The Section caps tariffs at 15% and limits them to 150 days unless Congress extends them and requires the tariffs to be applied on a nondiscriminatory basis, which reduces the administration’s flexibility compared to the previous IEEPA framework. In parallel, the administration signaled it would likely initiate new Section 301 investigations as a pathway to more targeted tariffs, while emphasizing that Section 232 and existing Section 301 tariffs remain in force.

In our view, the more immediate shift in tariff uncertainty is how ongoing trade pressures will manifest in the economy and corporate profits over the coming months and quarters, based on the Court’s ruling. Notably, the President’s inability to use the IEEPA tariff lever moving forward removes his most open-ended trade tool. Yet the administration was also prepared for this ruling and quickly pivoted to Section 122 as a stopgap measure to buy time to employ its tariff strategy under other Sections that appear more legally binding. However, it’s worth noting that the Court’s decision last week does not remove tariff uncertainty and may, in turn, dampen investment in some sectors as the White House seeks new and untested avenues to advance its trade agenda. With only a five-month global tariff in place and future trade barriers contingent on investigations, businesses must continue to navigate a fluid and uncertain global landscape. In our view, companies will remain cautious about capital spending and supply chain decisions in the interim, outside of AI-related investments.

Bottom line: The Congressional Budget Office estimated that the full scale of Trump’s tariffs was on track to bring in roughly $300 billion a year, which was an offset to the country’s continued deficit spending. Despite numerous studies, including one from the New York Federal Reserve last week, stating that U.S. consumers and businesses have shouldered the vast majority of the tariff costs, investors should expect the White House to find new ways to replace as much of that revenue as possible through other means. Thus, the tariff uncertainty continues with even less visibility moving forward.

The market braces for NVIDA's earnings update

Since the end of last year, Technology trade, particularly around artificial intelligence, has shifted from “show me the promise” to “show me the money”. Until late 2025, investors were broadly comfortable paying up for the largest AI platforms and hardware suppliers, on the assumption that demand would easily outstrip supply for the foreseeable future. In our view, that assumption largely remains intact, but the market’s tolerance for “spend now, benefits later” has tightened sharply this year, particularly against rising AI disruption fears. A simple way for investors to see this shift is through changes in market performance and leadership. For example, performance across Information Technology has cooled significantly since late December, and investors are increasingly rewarding companies that can show near-term cash generation and margin control alongside profit growth. Thus, the current earnings season has produced mixed stock reactions across mega-cap Tech. Although results have often been good enough on revenue and earnings relative to expectations, some Tech stocks have still struggled when management teams lay out enormous capital spending plans (e.g., Alphabet and Amazon) or when margin guidance implies that the AI buildout will pressure near-term profitability and free cash flow.

So, there stands the setup ahead of NVIDIA’s earnings report on Wednesday, which will likely play as the most influential report for broader markets this entire earnings season. NVIDIA’s results and outlook this week should provide a direct read-through on a key question inside the AI narrative right now: Are hyperscalers and large enterprises converting their aggressive AI infrastructure spending into near-term GPU and networking orders at the pace the market has been discounting? NVIDIA’s size, influence, and results will very likely amplify how investors view the answer to this question. Notably, the stock has become a large holding across the S&P 500 and the NASDAQ Composite, as well as growth allocations, which means its post-earnings move should influence sentiment well beyond the company and the semiconductor sector.

Similar to prior quarters, the bar for NVIDIA’s results and outlook on Wednesday is very high. According to FactSet, the chipmaker is expected to see roughly $65-$66 billion in revenue and about $1.50 a share in earnings for the prior quarter, implying another solid quarter of annualized growth. That said, investors will be looking for results that “surpass” expectations, accompanied by guidance that keeps the growth trajectory moving higher. Investors will also want to hear commentary from CEO Jensen Huang that reinforces that the supply chain and product ramps are supporting, not constraining, the company’s trajectory for growth. Importantly, we believe data center demand has to remain strong, and management needs to describe order patterns in a way that suggests spending is broad-based across hyperscalers and not overly dependent on a small set of near-term deployments and companies.

Additionally, execution on next-generation platforms, like Rubin, needs to give investors’ confidence that the company is on track with deployment schedules and that lead times are manageable. Finally, profit margin metrics could carry increasing influence this earnings season. Investors have shown they are willing to look through heavy spending in AI if they believe the payoff is visible and durable, but they have also demonstrated they will punish companies on any hint that pricing power is slipping or that costs related to ramping up supply are becoming a headwind.

Bottom line: NVIDIA’s results and message this week must reconcile two realities simultaneously: it needs to show that it's profitably benefiting from extraordinary AI demand today, probably above consensus estimates, while also demonstrating it can continue to successfully manage an industrial-scale manufacturing ramp not often seen in history. How investors reconcile these two realities could very likely dictate how the stock and broader averages perform post results. Given that the current market environment has shifted from celebrating the AI theme to auditing it, company results across Technology, including from Broadcom on March 4, will likely carry increasing weight as the cycle moves forward this year.

The week ahead:

- Along with NVIDIA’s earnings report on Wednesday, key retail reports from The Home Depot (Tuesday), Lowe’s (Wednesday), and TJX (Wednesday) will also be closely watched. Earnings from Salesforce, Intuit, and Autodesk could also capture the market’s attention this week.

- The economic calendar includes February consumer confidence on Tuesday and the January Producer Price Index on Friday.

- President Trump delivers his State of the Union address on Tuesday at 9pm EST.

These figures are shown for illustrative purposes only and are not guaranteed. They do not reflect taxes or investment/product fees or expenses, which would reduce the figures shown here. An index is a statistical composite that is not managed. It is not possible to invest directly in an index. Past performance is not a guarantee of future results.

Sources: FactSet and Bloomberg. FactSet and Bloomberg are independent investment research companies that compile and provide financial data and analytics to firms and investment professionals such as Ameriprise Financial and its analysts. They are not affiliated with Ameriprise Financial, Inc.

The views expressed are as of the date given, may change as market or other conditions change, and may differ from views expressed by other Ameriprise Financial associates or affiliates. Actual investments or investment decisions made by Ameriprise Financial and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances.

Some of the opinions, conclusions and forward-looking statements are based on an analysis of information compiled from third-party sources. This information has been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by Ameriprise Financial. It is given for informational purposes only and is not a solicitation to buy or sell the securities mentioned. The information is not intended to be used as the sole basis for investment decisions, nor should it be construed as advice designed to meet the specific needs of an individual investor.

Diversification does not assure a profit or protect against loss.

There are risks associated with fixed-income investments, including credit (issuer default) risk, interest rate risk, and prepayment and extension risk. In general, bond prices rise when interest rates fall and vice versa. This effect is usually more pronounced for longer term securities.

Stock investments involve risk, including loss of principal. High-quality stocks may be appropriate for some investment strategies. Ensure that your investment objectives, time horizon and risk tolerance are aligned with investing in stocks, as they can lose value.

Investments in small cap companies involve risks and volatility greater than investments in larger, more established companies.

Generally, large-cap companies are more mature and have limited growth potential compared to smaller companies. In addition, large companies may not be able to adapt as easily to changing market conditions, potentially resulting in lower overall performance compared to the broader securities markets during different market cycles

The products of technology companies may be subject to severe competition and rapid obsolescence, and their stocks may be subject to greater price fluctuations.

Past performance is not a guarantee of future results.

An index is a statistical composite that is not managed. It is not possible to invest directly in an index.

Definitions of individual indices and sectors mentioned in this article are available on our website at ameriprise.com/legal/disclosures in the Additional Ameriprise research disclosures section.

The S&P 500 Index is a basket of 500 stocks that are considered to be widely held. The S&P 500 index is weighted by market value (shares outstanding times share price), and its performance is thought to be representative of the stock market as a whole. The S&P 500 index was created in 1957 although it has been extrapolated backwards to several decades earlier for performance comparison purposes. This index provides a broad snapshot of the overall US equity market. Over 70% of all US equity value is tracked by the S&P 500. Inclusion in the index is determined by Standard & Poor’s and is based upon their market size, liquidity, and sector.

The NASDAQ Composite index measures all NASDAQ domestic and international based common type stocks listed on the Nasdaq Stock Market.

The Dow Jones Industrial Average (DJIA) is an index containing stocks of 30 Large-Cap corporations in the United States. The index is owned and maintained by Dow Jones & Company.

The Russell 2000 Index measures the performance of the small-cap segment of the US equity universe. The Russell 2000 is constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set. The Russell 2000 includes the largest 2000 securities in the Russell 3000.

The US Dollar Index (USDX) indicates the general international value of the USD. The USDX does this by averaging the exchange rates between the USD and major world currencies. This is computed by using rates supplied by approximately 500 banks.

West Texas Intermediate (WTI) is a grade of crude oil commonly used as a benchmark for oil prices. WTI is a light grade with low density and sulfur content.

The ISM Services PMI (formerly the Non-Manufacturing NMI) is compiled and issued by the Institute of Supply Management (ISM) based on survey data. The ISM services report contains the economic activity of more than 15 industries, measuring employment, prices, and inventory levels; above 50 indicating growth, while below 50 indicating contraction.

Personal consumption expenditures (PCE) are a measure of the outlays or how much consumers are spending. The PCE reading is released monthly by the Bureau of Economic Analysis.

Third party companies mentioned are not affiliated with Ameriprise Financial, Inc.

Investment products are not insured by the FDIC, NCUA or any federal agency, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities offered by Ameriprise Financial Services, LLC. Member FINRA and SIPC.

© 2026 Ameriprise Financial, Inc. All rights reserved.