Tech confidence is fading. What might trigger a broader market reset?

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — MARCH 2, 2026

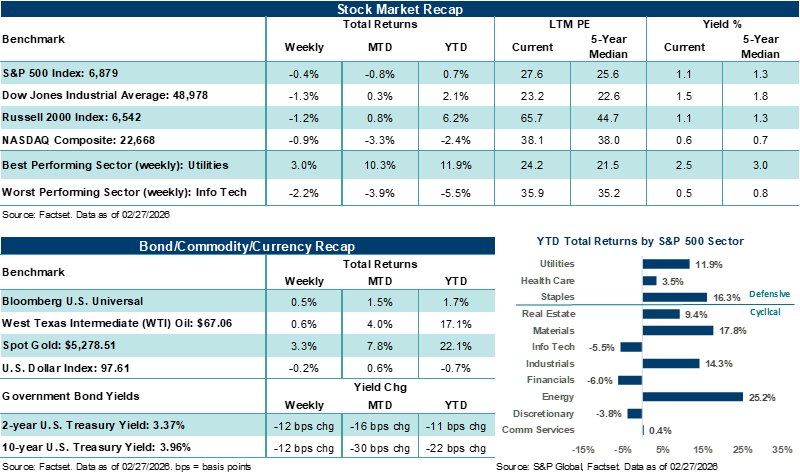

Major U.S. stock averages finished mixed in February, with the S&P 500 Index down for the second month in the last three, and the NASDAQ Composite posting its worst month since March 2025. On Saturday, the U.S. and Israel launched combat operations against Iran dubbed “Operation Epic Fury”. This week, investors will closely monitor developments in the Middle East and their impact on global oil supplies, as well as key U.S. economic data.

Last week in review:

- Major U.S. stock averages closed the last week of February lower. However, performance was mixed for the month, with the S&P 500 (-0.8%) and the NASDAQ (-3.3%) closing lower, while the Dow Jones Industrial Average (+0.3%) and the Russell 2000 Index (+0.8%) finished higher.

- AI disruption fears, a resulting large sell-off across Software, the Supreme Court striking down President Trump’s reciprocal tariffs, and rising U.S./Iran tensions weighed on stock prices last month. That said, economic data largely pointed to solid fundamentals in February, and S&P 500 fourth-quarter earnings came in well ahead of estimates.

- In February, U.S. Treasury yields fell, the U.S. Dollar Index strengthened, Gold jumped higher for the eighth straight month, and West Texas Intermediate (WTI) crude chopped higher on rising U.S./Iran tensions.

- Last week, January producer price inflation came in hotter than expected, with core prices hitting +3.6% on an annualized basis, the highest level since March 2025, due principally to rising trade services prices.

- On Saturday, the U.S. and Israel carried out coordinated air strikes against Iran, triggering a rapid response from Tehran that has expanded hostilities across Israel, US assets, and key Gulf states. In the initial minutes of the attack, Iran’s Supreme Leader Ayatollah Ali Khamenei and several top political and military officials were killed. In our view, the immediate risk for investors lies in how oil prices respond over the coming days and weeks, and if critical energy infrastructure and shipping lanes are disrupted. Expect markets to be laser-focused on potential supply risks, specifically in the Strait of Hormuz, potential OPEC+ responses, and knock-on effects in risk assets.

“The AI narrative has been a strong tailwind for U.S. stocks for many quarters and is currently going through a period in which disruption fears and spending and profit concerns among the Tech sphere have grown. However, a little doubt and worry, and maybe lower stock prices for a period, can be healthy after the run some of these stocks have seen. Frankly, it’s a normal part of the cycle during periods of rapid technological advancement.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

Tech confidence is fading. What might trigger a broader market reset?

Putting aside Middle East developments for a moment, market sentiment around AI spending, broader disruption fears from the technology and tie-ins to private markets around these factors continue to act as a wet blanket on broader averages. Not even positive earnings reports and outlooks from NVIDIA and Salesforce last week, or Amazon’s $50 billion investment into OpenAI, boosting the value of the privately held ChatGPT creator to $730 billion (up from $500 billion in October), were enough to shake investors’ sour mood on Tech. As such, investors appear more inclined to gravitate toward views pointing to potential worst-case AI scenarios for markets and the economy, which is causing significant churn beneath broader averages that continue to hold near highs. With that backdrop in mind, below is what we believe is a more sober assessment of some of the near-to-intermediate-term risks to AI, Big Tech, and broader markets that could stall the AI trade further but are unlikely to derail the longer-term opportunities across Tech.

- Overhyped Earnings & Valuations: As we have noted for some time, elevated valuations across AI-driven stocks leave little room for error at this point, despite still strong profit growth. Any earnings miss or a slowdown in growth relative to expectations could quickly erode investor confidence. For example, Microsoft’s Azure cloud growth decelerated slightly in the previous quarter, and margins fell as AI investments surged, triggering a sharp drop in the stock price despite otherwise solid results. The muted stock reaction to Salesforce’s solid results last week is another case in point. Such disappointments, if compounded across other tech companies, where expectations remain priced for perfection, could spark a broader selloff.

- Potential Overinvestment & Profit Squeezes: Big Tech giants are pouring unprecedented capital into AI. The largest hyperscalers plan to spend well over $600 billion in AI-related capex this year, a spend rivaling some nations’ budgets. This “AI arms race” boosts suppliers' profits today but could raise risks down the road if AI demand or returns on investment underwhelm. Thus, heavy spending could ultimately pinch margins more than expected, while the cost of AI buildouts increases unabated for a time. In an environment where AI costs are rising and margins are falling, the risk of declining stock prices rises.

- Potential Regulatory & Confidence Shocks: Sudden policy moves could deflate the AI boom. Possible triggers include stricter AI regulations (e.g., limits on data use or algorithmic accountability) that raise compliance costs, or antitrust actions that curb big players’ AI dominance. Likewise, an AI-related crisis, like a high-profile safety failure or data mishap, could quickly erode public trust and invite further regulatory scrutiny, abruptly tempering the market’s enthusiasm. Here, a more entrenched distrust of AI capabilities, or rising concerns about stricter regulation, could seriously temper AI enthusiasm.

- Macroeconomic Shift: A change in the economic backdrop can unexpectedly deflate stock momentum broadly, even across secular trends such as AI. For example, rising interest rates or a sustainable uptick in inflation could make richly valued AI stocks less attractive by raising the cost of capital and favoring safe-haven and defensive assets. Similarly, if economic growth slows more than expected, companies may trim discretionary spending on AI projects and IT, undermining the bullish revenue assumptions baked into many AI-driven stock prices.

Notably, we believe an AI sector pullback (under some of the conditions outlined above) would likely pressure earnings on multiple fronts. For example, companies that spent large sums of cash could face aggressive investor demands to quickly trim costs and improve free cash flow. And those whose business models are challenged by AI will be expected to adapt or shrink, potentially disrupting overall market momentum. Importantly, the exuberance that forgave short-term profit sacrifices over the last few years could evaporate, bringing a more unforgiving focus on quarterly results. In our view, there are already signs of this happening across Tech, as evidenced by underwhelming stock reactions following still-solid earnings reports over the last two seasons.

Additionally, under a much more extreme scenario than highlighted here, potential write-downs or project cancellations as companies admit that some AI initiatives won’t pan out as hoped would likely be greeted very poorly by the market, and analogous to the dotcom era, when telecoms wrote off fiber-optic investments. To be clear, this is not the environment we're in today, but it’s worth mentioning the point in a more bearish scenario. Conversely, companies that employed AI pragmatically, enhancing productivity without the need for unfettered spending, could shine in a more discriminating environment, as their return on investment becomes more valuable amid lowered expectations. Much like after the dotcom bust, when surviving internet companies finally became profitable, a more rational AI market would refocus on sustainability and cash generation, separating hope for the future from the reality of the day.

However, in a more likely downturn scenario over the next 6-12 months, we believe the AI trade would look less like a rupture and more like a healthy re-anchoring to fundamentals. As such, a more meaningful downturn in Tech (outside of what has already occurred in Software) might see investors increasingly gravitate toward companies with durable AI advantages, strong balance sheets, and credible monetization pathways. In that environment, we believe multiples can compress without the long-run opportunity disappearing. Seasoned investors often use dislocations to accumulate category leaders once prices stabilize, while weaker players struggle to regain peak valuations. We may already be seeing early signs of a market reset with an “orderly” rotation out of very crowded large-cap tech exposure and into the broader market areas. Of course, further weakness in Tech may precipitate a broader market selloff at some point, say a temporary 10%-15% drawdown in the S&P 500, which, admittedly, could feel uncomfortable for a period. But for the time being, renewed interest in Consumer Staples and Utilities, alongside non-tech cyclicals such as Industrials, Materials, and Energy, and international stocks, suggests that investors are still seeking opportunities where earnings and balance-sheet strength are visible, rather than running toward cash in fear.

Bottom line: The AI narrative has been a strong tailwind for U.S. stocks for many quarters and is currently going through a period in which disruption fears and spending and profit concerns among the Tech sphere have grown. However, a little doubt and worry, and maybe lower stock prices for a period, can be healthy after the run some of these stocks have seen. Frankly, it’s a normal part of the cycle during periods of rapid technological advancement. Thus, we believe it’s important to maintain a sober assessment in advance of what can go right and wrong during these historic market periods, which we believe can help investors avoid common portfolio pitfalls when and if conditions deviate from consensus thinking.

The week ahead:

- Roughly one-fifth of the world’s oil supply, including from Saudi Arabia, Iraq, and Iran, runs through the Strait of Hormuz. Traffic transiting the straight had already dropped off significantly before the strikes began this weekend. According to the U.S. Energy Information Administration, China receives roughly 38% of the crude that travels through the Strait, with India receiving 15%, and other Asian countries collectively accounting for 37%.

- Markets will likely be highly sensitive to oil prices this week as well as military developments. Over the intermediate term, a less stable Middle East, greater risk of attacks from Iran and its proxies in the region, and potential cyberattacks and other retaliatory responses against the U.S. and Israel could weigh on global asset prices for a period.

- That said, we believe investors are best served by standing pat for now and ensuring their portfolio is well diversified and aligned with their goals. Markets have a long history of eventually looking through geopolitical events once they can discount outcomes and determine longer-term economic impacts on growth and corporate profits.

These figures are shown for illustrative purposes only and are not guaranteed. They do not reflect taxes or investment/product fees or expenses, which would reduce the figures shown here. An index is a statistical composite that is not managed. It is not possible to invest directly in an index. Past performance is not a guarantee of future results.

Sources: FactSet and Bloomberg. FactSet and Bloomberg are independent investment research companies that compile and provide financial data and analytics to firms and investment professionals such as Ameriprise Financial and its analysts. They are not affiliated with Ameriprise Financial, Inc.

The views expressed are as of the date given, may change as market or other conditions change, and may differ from views expressed by other Ameriprise Financial associates or affiliates. Actual investments or investment decisions made by Ameriprise Financial and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances.

Some of the opinions, conclusions and forward-looking statements are based on an analysis of information compiled from third-party sources. This information has been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by Ameriprise Financial. It is given for informational purposes only and is not a solicitation to buy or sell the securities mentioned. The information is not intended to be used as the sole basis for investment decisions, nor should it be construed as advice designed to meet the specific needs of an individual investor.

Diversification does not assure a profit or protect against loss.

There are risks associated with fixed-income investments, including credit (issuer default) risk, interest rate risk, and prepayment and extension risk. In general, bond prices rise when interest rates fall and vice versa. This effect is usually more pronounced for longer term securities.

Stock investments involve risk, including loss of principal. High-quality stocks may be appropriate for some investment strategies. Ensure that your investment objectives, time horizon and risk tolerance are aligned with investing in stocks, as they can lose value.

Investments in small cap companies involve risks and volatility greater than investments in larger, more established companies.

Generally, large-cap companies are more mature and have limited growth potential compared to smaller companies. In addition, large companies may not be able to adapt as easily to changing market conditions, potentially resulting in lower overall performance compared to the broader securities markets during different market cycles

The products of technology companies may be subject to severe competition and rapid obsolescence, and their stocks may be subject to greater price fluctuations.

Past performance is not a guarantee of future results.

An index is a statistical composite that is not managed. It is not possible to invest directly in an index.

Definitions of individual indices and sectors mentioned in this article are available on our website at ameriprise.com/legal/disclosures in the Additional Ameriprise research disclosures section.

The S&P 500 Index is a basket of 500 stocks that are considered to be widely held. The S&P 500 index is weighted by market value (shares outstanding times share price), and its performance is thought to be representative of the stock market as a whole. The S&P 500 index was created in 1957 although it has been extrapolated backwards to several decades earlier for performance comparison purposes. This index provides a broad snapshot of the overall US equity market. Over 70% of all US equity value is tracked by the S&P 500. Inclusion in the index is determined by Standard & Poor’s and is based upon their market size, liquidity, and sector.

The NASDAQ Composite index measures all NASDAQ domestic and international based common type stocks listed on the Nasdaq Stock Market.

The Dow Jones Industrial Average (DJIA) is an index containing stocks of 30 Large-Cap corporations in the United States. The index is owned and maintained by Dow Jones & Company.

The Russell 2000 Index measures the performance of the small-cap segment of the US equity universe. The Russell 2000 is constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set. The Russell 2000 includes the largest 2000 securities in the Russell 3000.

The US Dollar Index (USDX) indicates the general international value of the USD. The USDX does this by averaging the exchange rates between the USD and major world currencies. This is computed by using rates supplied by approximately 500 banks.

West Texas Intermediate (WTI) is a grade of crude oil commonly used as a benchmark for oil prices. WTI is a light grade with low density and sulfur content.

The ISM Services PMI (formerly the Non-Manufacturing NMI) is compiled and issued by the Institute of Supply Management (ISM) based on survey data. The ISM services report contains the economic activity of more than 15 industries, measuring employment, prices, and inventory levels; above 50 indicating growth, while below 50 indicating contraction.

Personal consumption expenditures (PCE) are a measure of the outlays or how much consumers are spending. The PCE reading is released monthly by the Bureau of Economic Analysis.

Third party companies mentioned are not affiliated with Ameriprise Financial, Inc.

Investment products are not insured by the FDIC, NCUA or any federal agency, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities offered by Ameriprise Financial Services, LLC. Member FINRA and SIPC.

© 2026 Ameriprise Financial, Inc. All rights reserved.