The Warsh era begins as the Fed looks to maintain a tough stance on inflation

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — JUNE 15, 2026

U.S. stocks rebounded last week, snapping the prior week's selloff with broad-based gains and a notable rotation into small-caps and cyclicals. This week, the Federal Reserve's June meeting, May retail sales, and the G7 summit will be the key events to watch.

Last week in review:

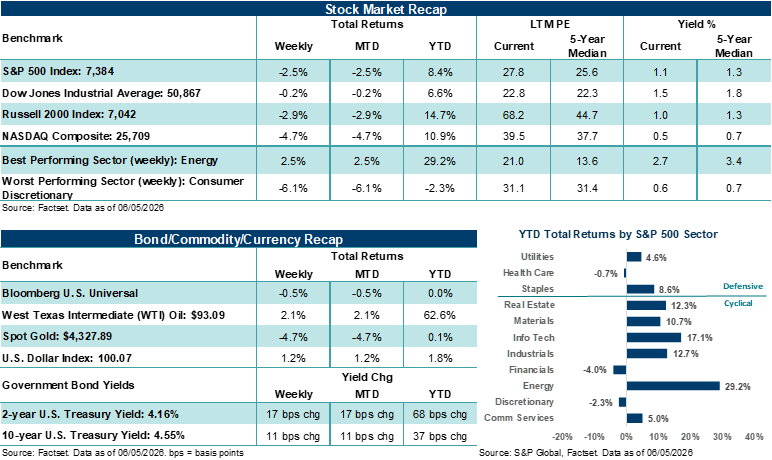

- The S&P 500 Index, NASDAQ Composite, and Dow Jones Industrial Average all rose +0.7%. The Russell 2000 Index was the standout, jumping +3.9% for its best week since mid-April. Notably, semiconductors rebounded sharply, with the Philadelphia Semiconductor Index rising +9.4%.

- Treasury prices firmed with the 30-year settling below 5.0%. The U.S. Dollar Index and Gold fell on the week, while West Texas Intermediate (WTI) crude dropped 10%, settling at its lowest level since mid-April.

- May inflation data came in mixed. Core CPI and core PPI both cooled from April levels, though headline readings remained elevated on energy prices. Initial jobless claims rose for a third straight week, while preliminary June consumer sentiment improved from May's record low.

- President Trump said Sunday that the U.S. and Iran reached a memorandum of understanding that would end the conflict and reopen the Strait of Hormuz. Oil prices moved lower last week as progress toward an agreement appeared imminent.

- SpaceX completed its roughly $75 billion IPO, with shares opening at $150 and trading +19% above the offering price. In the AI space, OpenAI reportedly filed confidentially for an IPO and reached one billion monthly users in May. Apple's WWDC keynote was generally viewed as underwhelming, with the stock falling 5.3% for the week.

- In our view, last week's rebound and broadening participation are encouraging signs that the market's foundation remains on solid footing. The rotation into small-caps, cyclicals, and financials suggests investors are finding opportunities beyond large-cap tech, even as the AI trade stabilizes.

“Bottom line: We believe the Fed will hold rates steady on Wednesday. That's the easy part. The three things that matter to markets this week include changes in statement language, the fate of the dot plot, and Warsh's debut press conference, where he sets the tone for how this Fed communicates going forward.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

The Warsh era begins as the Fed looks to maintain a tough stance on inflation.

The S&P 500 Index enters the week roughly 2.5% off its all-time high, following SpaceX's successful public debut on Friday. This week’s main event will come from Wednesday’s Federal Reserve decision and updated economic projections. Interestingly, the 2-year U.S. Treasury yield, at 4.08%, trades well above the 3.50%-3.75% fed funds band. And the preliminary June University of Michigan's long-run inflation expectations reading ticked lower to +3.4% last week from +3.9% in May but still sits well above where Fed officials would like to see it. So, while Wednesday's rate decision decisively points to a hold this week, everything that accompanies that outcome will be what investors focus on most.

Under normal circumstances, the case for a quiet meeting would be easy to make. A fed funds rate hold is currently priced at nearly 100% odds, so market expectations are set. New Fed Chair Kevin Warsh has no immediate mandate to move rates at his first meeting, so he doesn’t need to take action. And notably, core CPI at +2.9% in May gives the committee room to argue that higher headline inflation is energy-driven and temporary, potentially providing fodder for statement language this week. On paper, the Fed can stand pat, say little, and move on. In our view, that would be a pretty good outcome if that’s what happens this week.

Yet, in our view, three developments elevate this meeting beyond a routine hold-and-move-on outcome. First, the FOMC may remove its easing bias entirely from the policy statement. That could close a chapter of easing that began in Q3’24. As a result, the committee would no longer be signaling that the next rate move is more likely down than up. For the first time since the tightening cycle ended, the risk of higher rates could become symmetrical in the statement. Fed Governor Waller laid the groundwork publicly in May, arguing that "a rate cut is no more likely in the future than a rate increase." The April meeting included the most dissents since 1992, with several committee members moving toward a balanced rate approach. The June meeting could see more members take that view this week.

Second, the quarterly dot plot could come into focus on Wednesday more than usual as new economic projections are provided. Warsh has been a vocal critic of the forward guidance tool since former Fed Chair Ben Bernanke introduced it in 2012, arguing it anchors policymakers to stale forecasts. While we don’t expect he’ll eliminate it outright for this meeting, he may decline to submit his own dot, since it isn't required, or he may de-emphasize the projections in his press conference. As a result, we believe investors may need to start factoring in greater upside risks to rate volatility around FOMC meetings if the dot plot is ultimately eliminated or deemphasized by the Chair. Importantly, if investors lose the rate-path signal they've relied on for 14 years, the uncertainty premium could rise structurally. Thus, this week’s projections and how Warsh frames the dot plot could open the door to a meaningful change in how investors will have to interpret forward-rate policy under a new Chair.

If the dot plot remains informative at this week's meeting, the June projections should reflect a different picture than the March update. The March median dot of 3.4%, implying one 25 basis point cut from the current 3.50%–3.75% target range, now looks stale given how the inflation data has evolved. A shift in the median to 3.6% would signal the committee sees the easing cycle as effectively complete. A move to 3.9% would imply one 25-basis-point hike by year's end, which is basically where market expectations sit today (at least before news broke of a U.S./Iran memorandum of understanding on Sunday).

Third, inflation expectations are diverging from market pricing. A Michigan long-run inflation expectations reading of +3.4% sits at the upper end of the range since 2024. In May, fifty-seven percent of consumers cited high prices as eroding their personal finances. We believe inflation is causing real cracks among lower and middle-income households, and the persistence of that price pressure over multiple years is becoming a harder condition for the Fed to discount at current policy rates. Interestingly, inflation projections are likely to draw heavy scrutiny this week. The March headline PCE median of +2.7% was already a significant upward revision from December's +2.4%, yet the current Bloomberg consensus for full-year 2026 PCE sits at +3.6%, well above the committee's last projection. A further upward revision in the June inflation projections could signal that the committee views price pressures as more persistent than it had acknowledged just three months ago.

Then there’s Warsh himself. The new Fed Chair was nominated because he argued the Fed had room to cut rates. But coming into his first meeting as Chair this week, he faces headline CPI more than 2x the Fed’s target, a resilient job market, economic growth above trend, and a bond market signaling that rates are too low. At the same time, the White House still wants lower rates, though President Trump has, at times, publicly dialed back his rhetoric. And former Fed Chair Powell remains on the Board of Governors, the first former chair to do so since Marriner Eccles in 1948, citing ongoing legal matters and concerns over what he called unprecedented threats to the Fed's institutional independence.

In our view, investors will be watching closely how Warsh characterizes inflation in his press conference (i.e., temporary supply shock or broadening impulse), whether he offers any forward rate guidance at all, how he addresses the committee's divisions, any language on Fed independence, and whether he introduces his longer-term thesis that AI-driven productivity could justify lower rates. His framing this week will likely set the committee's reaction function for the rest of the year. However, we believe the current data has boxed him in for now, and the room for a dovish surprise is pretty narrow, at least for his first meeting.

Of course, a dovish surprise is always possible, even if the probability is low. Warsh could use the presser to signal patience, the dot plot could survive unbothered by Warsh’s personal views, and the statement could land softer than expected. But the weight of evidence points toward a hawkish tone shift by Fed officials this week. The European Central Bank hiked its policy rate for the first time since 2023 last week, with ECB President Lagarde warning that inflation is spreading beyond energy. Thus, the global rate landscape is evolving. The Fed is, by most measures, the last major central bank sitting on its hands. We believe the biggest risk heading into Wednesday is that the rules of the road that investors have grown accustomed to under previous Chairs may start to shift this week. And markets built on 14 years of forward guidance may need to learn to price a little more Fed uncertainty again. That said, this adjustment won't happen overnight. But the process may begin this week.

Bottom line: We believe the Fed will hold rates steady on Wednesday. That's the easy part. The three things that matter to markets this week include changes in statement language (easing bias likely dropped), the fate of the dot plot (de-emphasis likely), and Warsh's debut press conference, where he sets the tone for how this Fed communicates going forward. Notably, we see the committee moving toward a slightly more hawkish posture, even with the fed funds target range left unchanged. Importantly, investors should expect some changes in the Fed’s playbook and communication cadence over time as Fed Chair Warsh assumes the leadership role.

The week ahead:

- May retail sales on Wednesday will be the week's main economic release, offering the latest read on consumer spending amid elevated energy prices and softening sentiment.

- The G7 heads of state, including President Trump, will meet this week, with Iran negotiations and trade policy expected to be key agenda items.

Weekly Market Perspectives will be on hiatus for the next two weeks and return for the July 6th publication.

These figures are shown for illustrative purposes only and are not guaranteed. They do not reflect taxes or investment/product fees or expenses, which would reduce the figures shown here. An index is a statistical composite that is not managed. It is not possible to invest directly in an index. Past performance is not a guarantee of future results.

Sources: FactSet and Bloomberg. FactSet and Bloomberg are independent investment research companies that compile and provide financial data and analytics to firms and investment professionals such as Ameriprise Financial and its analysts. They are not affiliated with Ameriprise Financial, Inc.

The views expressed are as of the date given, may change as market or other conditions change, and may differ from views expressed by other Ameriprise Financial associates or affiliates. Actual investments or investment decisions made by Ameriprise Financial and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances.

Some of the opinions, conclusions and forward-looking statements are based on an analysis of information compiled from third-party sources. This information has been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by Ameriprise Financial. It is given for informational purposes only and is not a solicitation to buy or sell the securities mentioned. The information is not intended to be used as the sole basis for investment decisions, nor should it be construed as advice designed to meet the specific needs of an individual investor.

Diversification does not assure a profit or protect against loss.

Commodity investments may be affected by the overall market and industry- and commodity-specific factors, and may be more volatile and less liquid than other investments.

There are risks associated with fixed-income investments, including credit (issuer default) risk, interest rate risk, and prepayment and extension risk. In general, bond prices rise when interest rates fall and vice versa. This effect is usually more pronounced for longer term securities.

Stock investments involve risk, including loss of principal. High-quality stocks may be appropriate for some investment strategies. Ensure that your investment objectives, time horizon and risk tolerance are aligned with investing in stocks, as they can lose value.

Investments in small cap companies involve risks and volatility greater than investments in larger, more established companies.

Generally, large-cap companies are more mature and have limited growth potential compared to smaller companies. In addition, large companies may not be able to adapt as easily to changing market conditions, potentially resulting in lower overall performance compared to the broader securities markets during different market cycles

The products of technology companies may be subject to severe competition and rapid obsolescence, and their stocks may be subject to greater price fluctuations.

Past performance is not a guarantee of future results.

An index is a statistical composite that is not managed. It is not possible to invest directly in an index.

Definitions of individual indices and sectors mentioned in this article are available on our website at ameriprise.com/legal/disclosures in the Additional Ameriprise research disclosures section.

The S&P 500 Index is a basket of 500 stocks that are considered to be widely held. The S&P 500 index is weighted by market value (shares outstanding times share price), and its performance is thought to be representative of the stock market as a whole. The S&P 500 index was created in 1957 although it has been extrapolated backwards to several decades earlier for performance comparison purposes. This index provides a broad snapshot of the overall US equity market. Over 70% of all US equity value is tracked by the S&P 500. Inclusion in the index is determined by Standard & Poor’s and is based upon their market size, liquidity, and sector.

The NASDAQ Composite index measures all NASDAQ domestic and international based common type stocks listed on the Nasdaq Stock Market.

The Dow Jones Industrial Average (DJIA) is an index containing stocks of 30 Large-Cap corporations in the United States. The index is owned and maintained by Dow Jones & Company.

The Russell 2000 Index measures the performance of the small-cap segment of the US equity universe. The Russell 2000 is constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set. The Russell 2000 includes the largest 2000 securities in the Russell 3000.

The US Dollar Index (USDX) indicates the general international value of the USD. The USDX does this by averaging the exchange rates between the USD and major world currencies. This is computed by using rates supplied by approximately 500 banks.

West Texas Intermediate (WTI) is a grade of crude oil commonly used as a benchmark for oil prices. WTI is a light grade with low density and sulfur content.

The Philadelphia Semiconductor Index (SOX) is a stock market index that tracks the performance of companies in the semiconductor (chip) industry.

The Consumer Price Index (CPI) is an inflation indicator that measures the change in the total cost of a fixed basket of products and services, including housing, electricity, food, and transportation. The CPI is published monthly by the Commerce Department and is also commonly referred to as the cost-of-living index.

Producer Price Index (PPI) measures change in the prices paid to U.S. producers of goods and services. It is a measure of inflation at the wholesale level. The index is published monthly by the U.S. Bureau of Labor Statistics (BLS).

The Michigan long‑run inflation expectations reading is a survey-based measure from the University of Michigan that captures the median rate of inflation consumers expect over the next 5 to 10 years.

Personal consumption expenditures (PCE) are a measure of the outlays or how much consumers are spending. The PCE reading is released monthly by the Bureau of Economic Analysis.

Third party companies mentioned are not affiliated with Ameriprise Financial, Inc.

Investment products are not insured by the FDIC, NCUA or any federal agency, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities offered by Ameriprise Financial Services, LLC. Member FINRA and SIPC.

© 2026 Ameriprise Financial, Inc. All rights reserved.