It's time for corporate America to show its hand

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — APRIL 13, 2026

U.S. stocks climbed for a second straight week on ceasefire optimism, though the Strait of Hormuz remained largely closed, the Fed pushed back on near-term rate cuts and economic data pointed to a consumer under growing pressure. This week, the start of the Q1 earnings season will take center stage.

Last week in review:

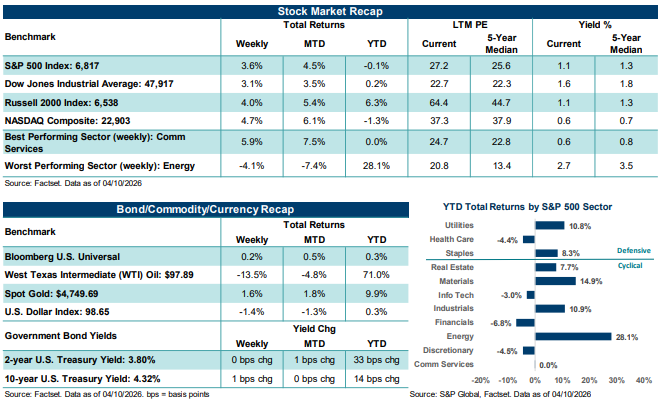

- The S&P 500 Index gained +3.6% and is now roughly 2.5% below its all-time closing high. The NASDAQ Composite and Dow Jones Industrial Average climbed +4.7% and +3.1%, respectively.

- U.S. Treasury yields were mixed, the U.S. Dollar Index fell, and Gold finished higher. West Texas Intermediate (WTI) crude settled down 13.5% for the week, its largest weekly decline since 2022, as ceasefire developments between the U.S. and Iran eased near-term energy supply fears.

- The largely upheld U.S./Iran ceasefire drove equity gains throughout the week. However, the Strait of Hormuz remained effectively closed. Only one tanker transited the Strait on Friday, and skepticism around permanent peace talks remained high given unresolved disagreements over Strait management and Lebanon's status.

- The March FOMC minutes leaned hawkish, with fewer officials projecting more than one rate cut in 2026 and Fed Chair Powell signaling that cuts depend on further core inflation progress. Inflation risks were seen skewed to the upside, partly due to oil, while the labor market was viewed as balanced but with downside risks.

- On the economic front, March core CPI came in slightly cooler than expected, though headline inflation was in line as energy prices jumped +10.9% and gasoline rose +21.2%, largely expected given the Iran conflict. February core PCE was in line, while personal spending rose +0.5% month-over-month, but personal income fell 0.1%, missing expectations for a 0.3% gain. The preliminary April University of Michigan consumer sentiment reading hit a record low, reflecting ongoing concerns about the conflict in Iran. A final read on Q4 GDP was revised lower to +0.5% from +0.7% on weaker investment, and February durable goods orders and factory orders were soft.

“The next few weeks of earnings updates and outlooks from corporate America should give investors an opportunity to reassess fundamentals against an evolving macroeconomic and geopolitical backdrop, particularly given the increasingly complex investing environment amid conflict in Iran and ongoing trade and tariff uncertainty.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

It’s time for corporate America to show its hand

The Q1 earnings season kicks off this week, with Goldman Sachs scheduled to report on Monday, followed by JPMorgan Chase, Wells Fargo, Citigroup, BlackRock, Johnson & Johnson on Tuesday, and Bank of America and Morgan Stanley on Wednesday. These early reports should offer some of the first meaningful looks at first-quarter consumer, business, capital markets and healthcare trends in the U.S., with management commentary likely to shape initial stock reactions to the reporting season. According to FactSet, analysts expect overall Q1’26 S&P 500 earnings per share (EPS) to grow by +12.6% year-over-year on revenue growth of +9.8%. If achieved, this would mark the sixth straight quarter of double-digit earnings growth and the highest revenue growth rate for the Index since Q3 2022.

Notably, despite a messier macro backdrop, we believe the earnings season begins from a constructive fundamental starting point, as profit and revenue expectations moved higher throughout the previous quarter, positive guidance was unusually strong, and overall margins, by historical standards, remain favorable. That said, the profit setup still appears narrower than the headline growth rate implies, with Technology and Communication Services expected to do much of the heavy lifting. At the same time, Healthcare and parts of the consumer complex saw expectations weakened over the quarter. As a result, the next few weeks of profit reports will likely need to confirm that earnings momentum is broad enough and guidance firm enough to support stock prices after a period of elevated volatility and, in some pockets, still above-average valuations.

One of the more favorable features heading into the current earnings season is that analyst estimates held up better than normal through the first quarter. Q1 S&P 500 EPS estimates increased by +0.4% from December 31 through early April. In addition, the Q1 bottom-up EPS estimate declined by just -0.3% during the previous quarter, compared with an average decline of -1.6% over the past five years and -2.9% over the past ten years, per FactSet. In our view, that tells investors two things. First, analysts did not materially de-risk their Q1 profit expectations. Second, companies entering the reporting season may not benefit from a meaningfully lowered earnings bar, which is historically par for the course. However, corporate guidance trends heading into the start of the season look favorable on the surface. According to FactSet, 110 S&P 500 companies issued quarterly EPS guidance for Q1, of which 59 issued positive guidance, and 51 issued negative guidance. Notably, this marks the highest percentage of companies issuing positive EPS guidance for a quarter since Q3’21. At the same time, 77 companies issued positive revenue guidance, which is the highest number since FactSet began tracking the metric in 2006. In our view, this positive preannouncement backdrop supports the idea that first-quarter operating conditions were generally favorable, a potential plus for stocks if confirmed over the coming weeks. However, it also means investors may be less willing to reward simple beats if forward guidance does not meet rising expectations.

Underneath the surface, Technology will likely remain the key driver of overall S&P 500 profit growth in Q1. The Information Technology sector is expected to report earnings growth of an eye-popping +45.1% year-over-year, the highest of all eleven S&P 500 sectors, on revenue growth of +27.4% year-over-year, also the strongest among all eleven S&P 500 sectors. At the industry level, all six Tech industries are expected to post year-over-year earnings growth, led by Semiconductors & Semiconductor Equipment at +95.0%. Importantly, if Semiconductors were excluded from the sector, expected Info Tech earnings growth would fall to +20.3%. In other words, the AI and semiconductor themes remain central to the overall earnings narrative, and results and guidance across large-cap Tech will likely play a significant role in shaping how investors judge the quarter as a whole.

Outside of Technology, Financials are also expected to provide notable support to first-quarter earnings growth. For example, Financials are expected to report earnings growth of +15.1% year-over-year and revenue growth of +10.0% year-over-year, with all five Financials industries projected to post annualized growth in both profits and sales. Given this week's reporting calendar, large banks and diversified financials should help set the early tone for the season. Investors will likely scrutinize commentary on net interest income, credit quality, deposit trends, trading activity, investment banking pipelines, and consumer credit behavior to determine whether Financials can validate the favorable sector-level setup.

That said, the positive first-quarter profit setup is not uniform across sectors. Healthcare is expected to report the largest year-over-year earnings “decline” of any sector at -9.8%. Consumer Discretionary has also weakened meaningfully, with expected earnings growth cut to +1.7% from +6.9% at the end of December, while Consumer Staples expected growth fell to +1.6% from +6.3%. However, all eleven S&P 500 sectors are still expected to post year-over-year revenue growth in Q1, suggesting top-line conditions likely remained broadly favorable. In our view, that likely leaves investors focused on operating leverage, cost control and guidance quality in these weaker sectors, rather than rewarding modest revenue beats alone.

Interestingly, profit margin trends could also remain supportive at the S&P 500 level. FactSet estimates that the S&P 500 net profit margin for Q1 could come in at +13.2%, equal to the prior quarter, above the +12.8% level a year ago, and above the 5- year average of +12.2%. Of course, Technology is expected to show the most meaningful margin improvement in Q1, with net margin estimated at +29.0%, up from +25.4% in the year-ago quarter. On the other hand, several sectors, including Healthcare and Materials, are expected to post margins “below” their own five-year averages. As a result, margin commentary during earnings calls should carry added importance this quarter, particularly for sectors where revenue growth held up but profits softened.

And on the valuation front, price-to-earnings multiples are less stretched than they were at the end of 2025. Yet companies in aggregate will likely still be required to show they are executing well in a complex environment. For example, the S&P 500 forward 12-month P/E ratio currently stands at 20.4x, which is slightly above the 5-year average, but down from roughly 22x at the end of the fourth quarter, reflecting both a lower Index price and higher forward earnings estimates. In our view, this could help reduce some valuation pressure heading into earnings season. Nevertheless, with earnings growth still expected to remain very strong over the next several quarters, companies will likely need to confirm that those expectations remain intact if stocks are to regain a firmer footing as the reporting season progresses.

Bottom line: The next few weeks of earnings updates and outlooks from corporate America should give investors an opportunity to reassess fundamentals against an evolving macroeconomic and geopolitical backdrop, particularly given the increasingly complex investing environment amid conflict in Iran and ongoing trade and tariff uncertainty. If the overall takeaway from the earnings season is that profits are strong, company execution is solid, and the outlook is positive, stocks could see a renewed tailwind. But if these areas show increasing cracks as the earnings season progresses, which is a distinct possibility across non-tech cyclicals, stock volatility could ramp back up. Every earnings season is important. And with all that the market has to contend with at the moment, the latest company report cards come at a time when investors are craving some fundamental certainty. However, asking for certainty in this type of investment environment might be asking a little too much, in our view. Solid results with mixed outlooks across a range of companies and industries might have to be enough for markets to go on until the next earnings update in July or macro conditions start to settle.

The week ahead:

- March small business optimism and producer price inflation on Tuesday, and the Fed’s Beige Book update on Wednesday, along with trade and housing data, will line the economic calendar amid corporate earnings reports.