If your 401(k) holds highly appreciated company stock, consider whether this little-known tax treatment can help lower your taxes.

If you’re close to retirement and have highly appreciated employer stock in your company’s 401(k), you may have a unique opportunity to lower your tax bill. Known as net unrealized appreciation (NUA), this tax treatment is a complex, one-time-only opportunity that can provide benefits, but it also comes with specific requirements and several tradeoffs.

An Ameriprise financial advisor can work with your tax professional to help you determine whether you might qualify for and benefit from this tax treatment.

What is net unrealized appreciation?

Within the tax code, NUA is the difference between the original value of an employer stock (its cost basis) and its current market value.

For example, if 100 shares of company stock were put into your plan five years ago at $10 per share, your cost basis would be $1,000. If the current price of the shares is $25 each, the total market value is now $2,500. The difference between the cost basis and current market value of your company shares is your NUA, which in this case is $1,500.

How is NUA taxed?

Under ordinary circumstances, when you take distributions from a retirement account like a 401(k), both the original value of the assets in the account and the appreciation amount are taxed as ordinary income.

However, the tax code treats NUA differently. The appreciation of the stock is taxed at the more favorable capital gains tax rate, which — depending on how much stock you own and how much it has appreciated — can potentially result in substantial tax savings.

Net unrealized appreciation calculator

Use this tool to see if a NUA tax strategy could benefit your retirement savings.

What is the NUA tax strategy?

When you want to take employer stock out of your 401(k) or other employer-sponsored retirement plan, you will face a choice: roll it into an IRA or move it into a taxable account.

When you take a lump-sum distribution1 from your employer-sponsored retirement plan, you’ll generally pay ordinary income tax on the current market value of those assets, plus any cash distributed. However, you may be able to pay taxes at the lower capital gains rate on portions of that lump-sum distribution if you are eligible.

If you have employer stock in your qualified account that has grown significantly in value, you may be able to take advantage of net unrealized appreciation by taking a lump-sum distribution and then transferring the employer stock in-kind2 to a taxable brokerage account.

Because the federal long-term capital gains rate is generally lower than ordinary income tax rates, the net unrealized appreciation strategy may significantly reduce your tax burden.3 However, while you may pay less in taxes on the net unrealized appreciation when you sell the stock, the cost basis will be subject to taxation at ordinary income tax rates in the year you take the distribution.4

How the NUA tax strategy works

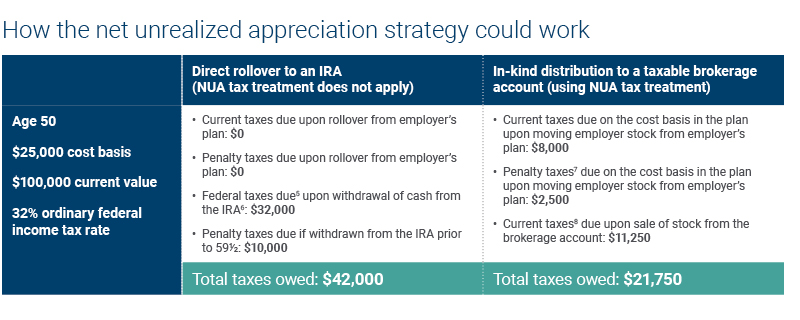

To better understand how NUA may be financially advantageous, consider the following scenario:

The above hypothetical, highly simplified example compares the tax treatment of a direct rollover to moving highly appreciated employer stock in-kind as part of a lump-sum distribution. Other assets are rolled into an IRA in this example.

What are the NUA rules and requirements?

To take advantage of the NUA tax treatment, there must be a triggering event, which includes turning 59½, leaving your employer, death or disability. Once the triggering event happens, other circumstances must be in place for the stock to qualify for NUA treatment:

-

The stock must be in a tax-deferred retirement account such as a 401(k) — it can’t be in a tax-exempt vehicle such as a Roth IRA or Roth 401(k).

-

If the stock is in a mutual fund account, the fund can only include company stock or cash. (Stock from other companies disqualifies the fund’s eligibility for NUA.)

-

The entirety of the retirement account must be distributed in the year you execute the NUA strategy.

-

The company stock needs to be taken out of the retirement account and placed in a non-qualified brokerage account while the remaining assets can be rolled into an IRA. Once the lump-sum distribution is complete, your tax professional can use the NUA treatment for the employer stock.

Who may benefit from a NUA tax strategy?

The NUA tax treatment can be highly complicated to execute and who could benefit will depend on their unique financial circumstances. That said, it’s more likely to be advantageous in the following scenarios:

-

If you have highly appreciated employer stock: Generally, the larger the difference in value between the cost basis and the current market value of the stock, the more potential tax benefit you’ll see with a NUA strategy. For that reason, it’s a good idea to verify the accuracy of your cost basis information with your retirement plan sponsor.

-

If you are in a lower tax bracket than usual: At the time you take any lump-sum distribution from a retirement plan, you will incur a tax bill for the cost basis at your ordinary income tax rate. If you wait until you’re in a lower tax bracket (for example, in the early years of retirement) to use the NUA strategy, it could help lessen that tax bill. You will also pay taxes on the rest of the distribution unless you roll it over to an IRA.

What are different ways to implement the NUA tax strategy?

There are a few different ways you can implement the NUA tax strategy for maximum benefit. What path is right for you will depend on your personal financial situation, risk tolerance and time horizon.

-

Keep your employer stock after NUA: By holding onto your employer stock for years after you execute a NUA strategy rather than selling it at the time of the lump-sum distribution from the employer plan, you may potentially benefit from a longer runway of tax-deferred growth.

-

Sell the stock immediately, or in small increments, over the following years: This can effectively give you a distribution from the plan that is at the lower long-term capital gains rate, rather than at the generally higher ordinary income tax rate.

-

Distribute only a portion of the stock: You don’t have to distribute all your employer stock to take advantage of the NUA tax treatment. You can use some for NUA and roll over the rest into an IRA, where it can be diversified into other investments without a tax consequence. The IRS allows you to select batches of employer stock for the most favorable cost basis for NUA purposes provided your 401(k) (or other employer-sponsored plan) has documented the purchases and recorded the cost basis of the employer stock over the years.

-

Let your heirs benefit from NUA: If you have not sold the employer stock before you die and your beneficiaries meet the requirements, they may also use the NUA tax strategy. Just note that the NUA portion of the stock will not be eligible for a step-up in basis.

Get personalized advice for complex questions

If you own company stock in an employer-sponsored retirement plan, connect with your Ameriprise financial advisor before you roll it over to an IRA. They can work with your tax professional to evaluate whether the NUA strategy fits your situation and financial goals.

One of your clients has some questions they would like to discuss with you at your next meeting.

warning Something went wrong. Do you want to try reloading? Try again

When you’re ready to reach out to an Ameriprise financial advisor for a complimentary initial consultation, consider bringing these questions to your meeting.

Reach out to %advisor% to start the conversation.

Or, request an appointment online to speak with an advisor.

At Ameriprise, the financial advice we give each of our clients is personalized, based on your goals and no one else's.

If you know someone who could benefit from a conversation, please refer me.

Background and qualification information is available at FINRA's BrokerCheck website.