Protecting your earned income with disability insurance and life insurance

Help protect your family’s financial future in the event of disability or death with these insurance solutions.

For most people, the ability to earn income is among their most significant financial assets. And if you suddenly couldn’t work due to death, illness, accident or injury, your family’s financial future could be at risk. Even a temporary loss of income could substantially impact your savings, retirement plans and other goals.

An Ameriprise financial advisor can help you find solutions that can add a layer of protection by helping to protect your income if something unexpected happens.

Here’s what to know about disability insurance and life insurance as a form of income protection.

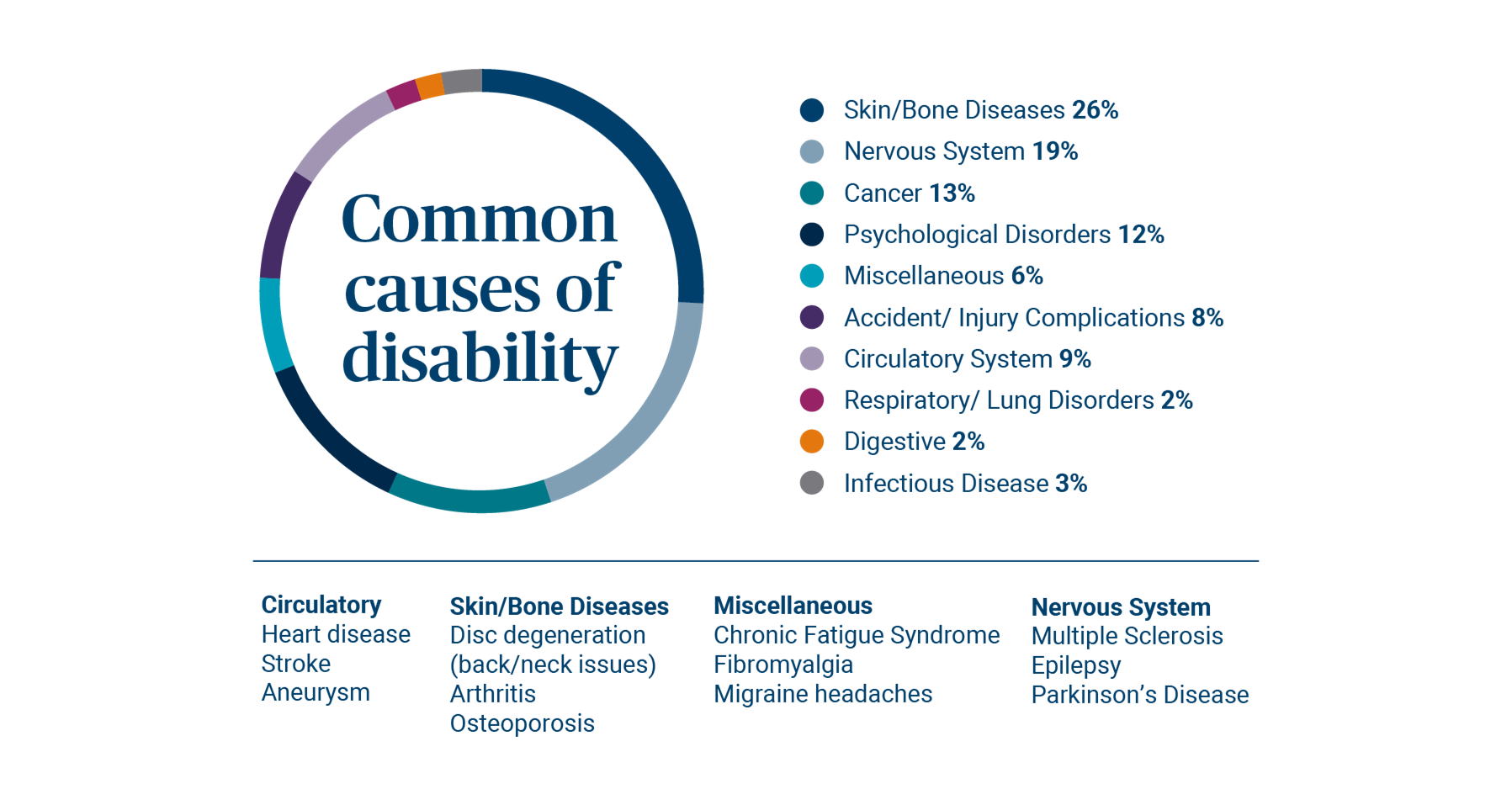

Disability income insurance

What is it? Disability income insurance is like having insurance for your paycheck. If an injury or illness prevents you from working, it replaces a percentage of your earned income to help you pay your bills and maintain your lifestyle.

Who is it for? Anyone who relies on their earned income to pay expenses and save for future goals.

Why is disability income insurance needed? Disability income insurance can protect your income during your core earning years — when any interruption could substantially impact your ability to pay your bills and save for your goals. Many people can elect coverage through their employer as part of an employer-sponsored group plan. Group disability income insurance often offers affordable coverage, but typically only covers 60%1 of your salary and may not cover bonuses, commissions and retirement plan contributions. In addition, for most employer-based plans, as soon as your employment ends, so does your coverage.

An individual disability income insurance policy can provide additional coverage if you are self-employed or offer supplemental coverage to your group plan.

If you have a group policy through work, adding an individual policy allows you to:

- Make up for a portion of your income not covered by group insurance benefits

- Have coverage if you change jobs

- Customize the coverage to include annual cost-of-living adjustments

Source: RiverSource Life disability insurance claims payments through Dec. 31, 2022. The above is for illustrative purposes only and is not intended to be an inclusive representation of all claims.

How much does disability income insurance cost? Generally, it costs 2 to 3% of a person’s salary to cover up to 80% of their after-tax income during a disability.1 The following factors may also affect your cost:

- Age

- Gender

- Occupation

- Length of waiting period (also known as the elimination period)

- Length of benefits

- How the policy defines disability

One of your clients has some questions they would like to discuss with you at your next meeting.

warning Something went wrong. Do you want to try reloading? Try again

When you’re ready to reach out to an Ameriprise financial advisor for a complimentary initial consultation, consider bringing these questions to your meeting.

What are other considerations with disability income insurance? When looking at plans, consider:

How the policy is paid out: Some policies pay out only if you can’t work any job for which you’re qualified, while others pay out if you can’t perform a job in your occupation. Some policies will pay a benefit if you can work part-time, while others only pay if you can’t work at all.

How much coverage you can purchase: An insurer will consider other sources of disability insurance to determine how much coverage you can buy and will typically cover up to 80%1 of your after-tax income during. However, because you will pay for any individual coverage with after-tax dollars, the income from those benefits is typically tax-free should you become disabled.

Life insurance

What is it? In the event of your death, life insurance can help replace your income so your loved ones can continue to maintain their quality of life and fund future goals. Income replacement is a main reason many people have life insurance coverage.

Who is it for? Anyone with dependents – children, a spouse or partner, parents or other relatives. Life insurance helps to protect the value of your future income, as well as the value of support you provide for your family that would otherwise have to be paid for (for example, childcare, home maintenance, etc.). That’s why life insurance is equally important for stay-at-home parents and caregivers who provide a large support role for the family.

Why is life insurance needed? In the event of your death, your policy’s payout typically goes directly to your beneficiaries, who can use it to cover costs in your absence, whether that’s daily expenses, a mortgage, childcare, higher education or a partner’s retirement.

How much life insurance do I need? Each person’s situation is different, but for income replacement a common starting point is to multiply your annual salary by the number of years you desire to have coverage. Beyond that, account for additional expenses like debt, a child’s college education, rising living expenses and burial costs.

Term or permanent life insurance? When purchasing life insurance, you have many options, but one key choice is deciding if you want term life insurance or permanent life insurance. Both help ensure your dependents are financially cared for if you were to pass away unexpectedly, but there are major differences, so evaluate which policy type or combination of policy types will suit your needs.

A new report from Ameriprise Financial finds that those who are single, divorced and widowed feel empowered in managing their finances, yet there are opportunities to strengthen their protection against risk.

Protect your income and financial future

Talk to your Ameriprise financial advisor about the disability and life insurance options available to protect your income and how to tailor coverage to help meet your specific needs.

RELATED INFORMATION

Or, request an appointment online to speak with an advisor.

At Ameriprise, the financial advice we give each of our clients is personalized, based on your goals and no one else's.

If you know someone who could benefit from a conversation, please refer me.

Background and qualification information is available at FINRA's BrokerCheck website.